In disruption reviews across battery and magnet supply chains, the break rarely appears at the mine gate. It usually appears later, when a concentrate with acceptable grade cannot be converted into a qualified chemical, separated oxide, sulfate, or anode material on the timetable assumed by downstream plants. That operating reality explains why critical minerals refining carries more geopolitical weight than mine ownership alone.

- Commonly cited public estimates place China at around 90% of rare earth separation, about 60-70% of lithium chemical refining, and roughly 75-80% of cobalt refining, alongside a dominant position in graphite anode material processing.

- The recurring chokepoint is not geology by itself, but conversion: solvent extraction, purification, precipitation, crystallization, spheronization, coating, and qualification.

- Mine headlines can overstate resilience. A new source of feedstock does not remove dependence if the material still travels into Chinese conversion plants or precursor lines.

- Observed failure modes cluster around impurity control, reagent and utility dependence, environmental permitting, residue handling, and slow downstream qualification.

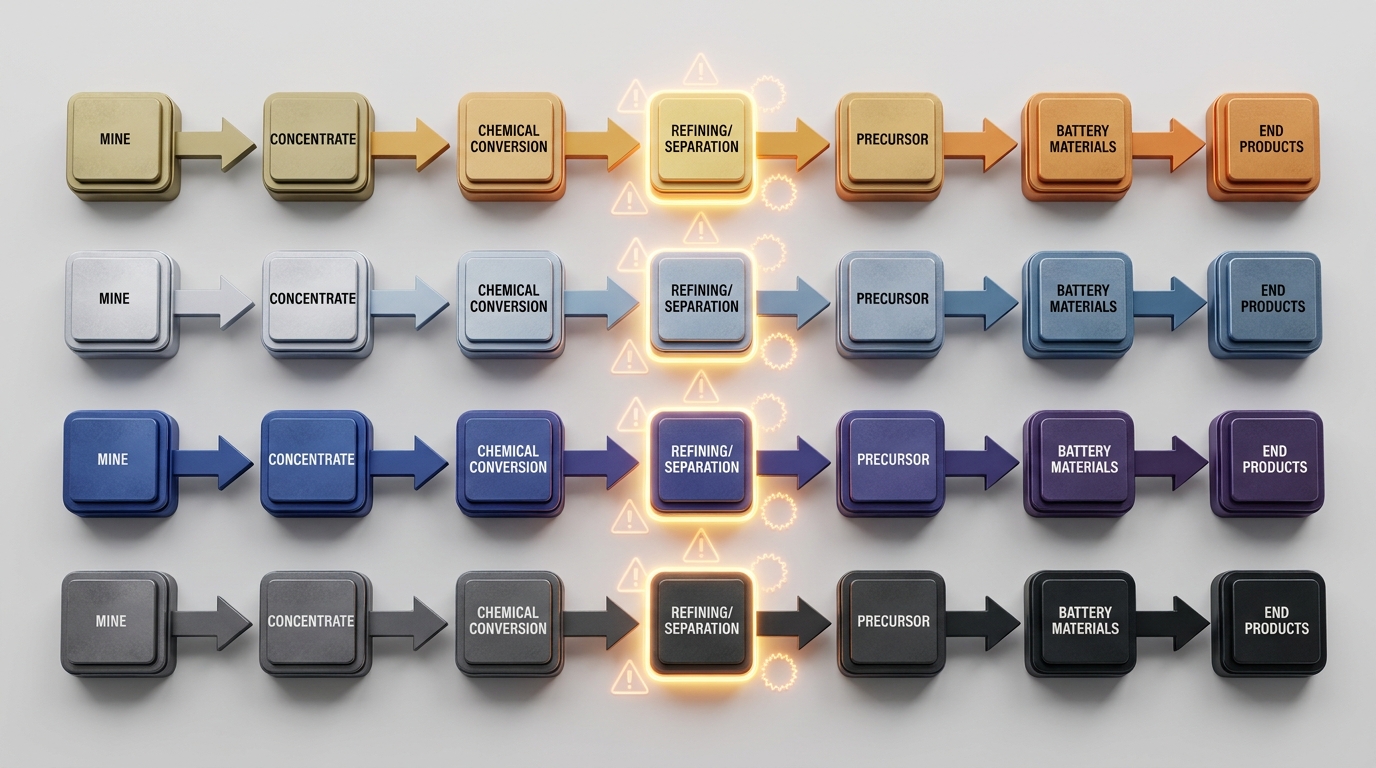

Why refining defines control more clearly than mining

Mining creates feedstock. Refining creates usable material. Between those two points sits the industrial layer that removes impurities, separates chemically similar elements, controls particle morphology, and produces the exact specification a battery, magnet, alloy, or electronics manufacturer can qualify. In practice, that layer is often the hardest part to replicate because it depends on cumulative process know-how, stable utilities, high-purity acids and reagents, compliant waste treatment, and customers willing to qualify output at ppm, or parts-per-million, impurity thresholds.

A recurring discovery in operational assessments is that mine-level metrics such as TREO grade in rare earths or LCE headlines in lithium say less than expected about resilience. TREO, or total rare earth oxides, can look attractive while the distribution of magnet rare earths and the burden of separation remain unfavorable. LCE, or lithium carbonate equivalent, can signal scale at the resource level while conversion into battery-grade hydroxide or carbonate remains constrained elsewhere. The center of gravity shifts from resource abundance to process capability.

How the chokepoint appears in four mineral chains

Rare earth refining shows the pattern most clearly. China rare earth processing retains the dominant position in separation, with public estimates commonly clustering around 90% of global separation capacity. That share matters because mined mixed rare earth concentrate is not yet a magnet input. The difficult step is separating near-identical lanthanides through long solvent extraction circuits, then converting selected oxides into metals, alloys, and magnets. In practice, a rare earth mine outside China can still leave the system dependent on Chinese separation if no alternative route exists for NdPr and heavier elements such as dysprosium and terbium.

Lithium refining follows the same logic. Spodumene concentrate from Australia or brine-derived intermediates from South America do not directly supply a cathode plant. They first move through chemical conversion into battery-grade lithium carbonate or lithium hydroxide. Public estimates often place Chinese lithium refining in the 60-70% range, with variation by product and reporting year. A common discovery during supply-chain reviews is that mine commissioning receives more attention than conversion ramp-up, yet qualification failures in lithium refining can delay usable output even when mined feedstock is available.

Cobalt refining adds a different layer of concentration. Mine production is tied heavily to copper and nickel systems, especially in the Democratic Republic of Congo, but refining into battery-grade cobalt sulfate is concentrated in China. Public estimates commonly place China’s cobalt refining share around 75–80%. The operational choke point is purification and crystallization to a specification accepted by precursor manufacturers. Traceability, jurisdictional risk, and transport complexity matter, but chemical conversion remains the decisive point where feedstock becomes usable battery material.

Graphite is often underestimated because the strategic issue is farther downstream than mining. Battery makers do not consume flake graphite as-mined. They consume anode material: purified spherical graphite, coated spherical graphite, or synthetic graphite products meeting demanding morphology and purity standards. China dominates graphite anode material refining through purification, spheronization, coating, and integration with battery-material manufacturing. This is one of the clearest examples of a chain where new mining outside China does not, by itself, solve the bottleneck.

Why China dominates critical minerals refining

The concentration is not explained by geology alone. China built durable advantages in process industries that become stronger with repetition and scale. Solvent extraction circuits in rare earth refining, impurity control in lithium refining, sulfate production in cobalt refining, and anode finishing in graphite all benefit from years of plant learning. The more often a plant solves filtration issues, reagent balance problems, residue handling, or product-spec drift, the harder it becomes for a new entrant to match consistency.

Industrial clustering also matters. Refining plants operate more reliably when acids, alkalis, reagents, power, water treatment, waste disposal, laboratories, and downstream customers sit within the same industrial ecosystem. China assembled those ecosystems around magnets, cathodes, precursor materials, anodes, electronics, and electric-vehicle manufacturing. That clustering shortened the distance between chemical conversion and final qualification. It also reduced the operational penalty when a process line needed troubleshooting or a product needed reformulation for a specific customer.

Another discovery from actual supply disruptions is that documentary readiness can be as important as metal content. Export controls, customs classifications, chain-of-custody declarations, safety data sheets, environmental permits, and traceability files can interrupt shipments even when physical production is available. China’s mature processing base often sits inside established documentation routines for these flows, whereas emerging plants in other jurisdictions may still be building those systems.

Why Western mining projects do not remove the dependence

The phrase “mine supply” can obscure where vulnerability actually sits. A lithium mine in Australia, a rare earth project in the United States, a graphite mine in Africa, or a cobalt source outside China improves optionality at the feedstock level. It does not automatically create separated oxides, battery-grade lithium chemicals, cobalt sulfate, or coated spherical graphite in the same jurisdiction. If those conversion steps still occur in China, dependence remains embedded in the chain.

This gap appears repeatedly when upstream projects reach production before downstream refining is ready. Concentrate can be shipped, but product qualification lags. Residue management systems may still be under review. Reagent purity or utility stability may not match process assumptions. In rare earths especially, the route from mine concentrate to separated oxides and then to magnet metal is long enough that one missing processing stage can preserve the original chokepoint almost intact.

Assessment frame: the signals that matter in refining risk

A practical assessment of critical minerals refining usually turns on five layers. The first is process complexity: the number of stages between feedstock and final specification, including solvent extraction, roasting, leaching, precipitation, crystallization, purification, calcination, spheronization, and coating. The second is dependency on inputs such as sulfuric acid, caustic soda, specialty reagents, water quality, and uninterrupted power. The third is environmental and residue management, since wastewater, tailings, fluorine-bearing streams, or other by-products can become the real source of delay.

The fourth layer is qualification risk. Battery, magnet, and specialty-alloy manufacturers often require long validation cycles before new material enters a production line. A refinery can so exist physically while remaining commercially irrelevant to the downstream system if output is not yet qualified. The fifth layer is route concentration: whether a material flow still depends on one country, one processing cluster, one port, or one customs channel. Australia-to-China spodumene flows and Congo-to-China cobalt intermediate flows illustrate how mining diversity can coexist with refining concentration.

Observed failure modes are also fairly consistent across minerals. Product purity can drift outside accepted ppm limits. Recovery rates can vary by feedstock blend. Waste circuits can limit throughput before the core chemical line does. Qualification can fail because particle size distribution, morphology, or trace contaminants differ from an incumbent supplier’s output. Documentary gaps can hold cargo even when plant operations are stable. These are refining problems, not mining problems, and they often determine whether a nominally diversified chain is truly resilient.

Observed responses in practice

Across jurisdictions, several management patterns have appeared without eliminating the underlying difficulty. Some chains pursue integrated mine-to-chemical projects so that feedstock and conversion develop together. Others build partial regional capacity first, such as mixed rare earth carbonate processing, intermediate lithium conversion, or graphite purification ahead of full anode production. Some systems rely on allied-country processing networks rather than a single domestic site. Recycling and scrap recovery also appear more often in planning because they can supply refined units with less exposure to raw feedstock concentration, although recycled streams still require sophisticated separation and purification.

Catch-up outside China looks most plausible where an existing chemical industry, stable utilities, waste-treatment infrastructure, and downstream manufacturing already coexist. Even then, the hard part is consistency rather than construction alone. A refinery can be commissioned long before it becomes a trusted source for a cathode line, a magnet producer, or an anode plant. That distinction is central to any reading of critical minerals refining: capacity on paper and qualified supply in practice are not the same thing.

The hidden bottleneck, then, is not hidden because it is obscure. It is hidden because mining still dominates the public narrative while refining determines the practical balance of power. In lithium, rare earth refining, cobalt refining, and graphite anode material processing, the decisive leverage sits in conversion, separation, and qualification. That is where concentration persists, where disruptions spread fastest, and where supply-chain resilience is either confirmed or disproved.