In rare earth supply reviews, the first discovery is often physical rather than chemical: end-of-life products rarely appear as a clean, labeled magnet stream. A hard disk drive may yield a recognizable NdFeB magnet, while mixed electronics often arrive shredded, glued, coated, and undocumented. That gap between theoretical metal content and usable feedstock explains both the appeal and the frustration of rare earth recycling. For professional due-diligence work in rare earths and magnet metals, including family-office research functions, private-wealth due-diligence teams, OEM sourcing groups, and industrial strategy desks, recycling is best understood as a risk-mitigation layer rather than a full substitute for primary mining.

Key takeaways

- Rare earth recycling is technically feasible, especially for NdFeB recycling from magnets, but feedstock quality and collection control usually matter more than headline recovery rates.

- Industrial scrap and clearly identified magnet waste tend to be the most reliable recycling streams; dispersed consumer electronics remain the hardest to aggregate and sort.

- Urban mining can diversify NdPr supply over time, yet near-term dysprosium recycling and terbium recovery remain constrained by low concentrations, separation complexity, and limited end-of-life volume.

- Wind turbines and EV motors represent meaningful future feedstock, but much of that volume arrives later, as fleets age and repowering cycles accelerate after 2030.

- Traceability, mass balance, and downstream refining capacity often determine whether a recycling claim is operationally credible.

Where the urban mine is real

The urban mine for rare earths is not a single pool of material. It is a patchwork of waste streams with very different handling requirements. The most relevant sources for rare earth recycling are permanent magnets recovered from decommissioned hard disk drives, speakers, headphones, industrial motors, and manufacturing scrap; EV motors and powertrains that reach end of life as the fleet ages; wind turbine generators removed during repowering or decommissioning; phosphor-bearing fluorescent and LED lighting; and smaller amounts embedded in smartphones, digital cameras, and other consumer electronics. Industrial scrap usually stands apart because composition is better known and the material is already concentrated.

Scale looks compelling on paper. Wind turbines can contain roughly 600 to 2,000 kilograms of permanent magnet material per unit, and EV traction motors commonly carry around 1 to 3 kilograms of magnet material. Yet availability in a spreadsheet is not the same as availability at a recycler gate. Global rare earth recycling is still often cited at roughly 1% of supply, and only about one-fifth of e-waste is collected and recycled at all. In practice, urban mining rare earths works best when the stream is concentrated, identifiable, and physically recoverable without destroying the magnet before separation begins.

Can rare earth magnets be recycled?

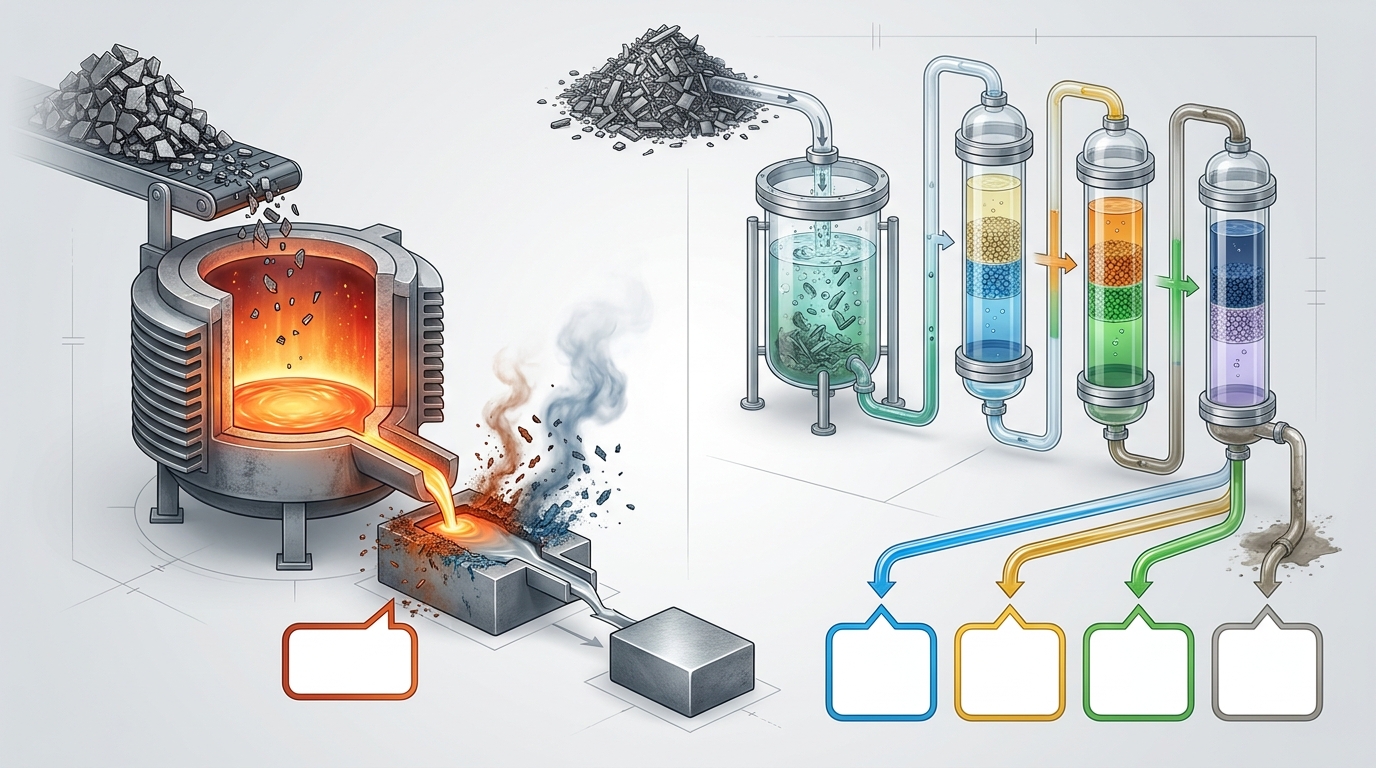

Yes. Permanent magnets can be recycled through two broad routes. The first is direct or “magnet-to-magnet” recycling, where NdFeB magnet material is recovered, cleaned, degaussed, processed, and reintroduced into magnet manufacturing with limited chemical breakdown. This route can preserve alloy value and reduce some processing intensity when magnet grade is known and contamination is controlled. The second route is hydrometallurgical processing, where the magnet is dissolved and the rare earth elements are separated chemically into purified streams such as neodymium, praseodymium, dysprosium, and terbium.

Each route carries trade-offs. Direct recycling is attractive for homogeneous production scrap and clearly identified returned magnets, but mixed grades, nickel coatings, copper layers, epoxy, oxidation, and adhesive residues can quickly degrade the result. Hydrometallurgy is more flexible when feedstock is dirty or mixed, and it can produce high-purity separated material, but it adds reagent handling, residue treatment, and tighter chain-of-custody demands. One recurring discovery in recycling assessments is that shredding simplifies bulk e-waste handling while simultaneously destroying the identity of the most valuable magnet-bearing components. Once that identity is lost, recovery becomes a chemistry problem instead of a controlled materials problem.

Why is rare earth recycling still small?

The limiting factor is usually not laboratory chemistry. It is the feedstock system around the chemistry. Collection remains fragmented across jurisdictions, product categories, and disposal habits. Rare earth-bearing goods are often discarded as part of larger equipment assemblies, and the magnet is rarely tracked as a separate component. Under the EU WEEE regime, collection and recycling targets exist for broad equipment categories, but rare earth recovery has historically not been the central design feature. As a result, much collected material enters bulk metal recovery pathways rather than dedicated rare earth separation.

Disassembly adds another bottleneck. Consumer devices hide tiny magnets in compact assemblies. EV motors can require specialist teardown. Wind turbine generators contain larger and more accessible magnet masses, yet logistics, handling, and degaussing introduce their own operational burden. In higher-cost jurisdictions, manual separation can absorb much of the value before refining begins. Traceability is another frequent weak point. Credible recycling claims are usually supported by some combination of bill-of-materials data, teardown protocols, serial-number linkage, assay reports, mass-balance records, and downstream refining certificates. When those records are thin, “recycled rare earth” can mean almost anything from clean production scrap to low-grade mixed residues.

The economics gap: where claims often break down

Economics in magnet recycling are strongest when feedstock is concentrated, known, and already inside an industrial loop. They weaken when the stream is dispersed, contaminated, or compositionally uncertain. Recovery percentage on its own is rarely enough to establish commercial relevance. The more important question is whether the recovered output can return to the magnet value chain in a specification that alloy makers and magnet manufacturers can actually use. A process that produces a mixed rare earth concentrate or low-value chemical intermediate may recover metal, but it does not necessarily reduce strategic supply risk in the same way as qualified magnet feedstock.

- Observed failure mode: feedstock mismatch. A plant designed for clean NdFeB scrap receives mixed e-waste fractions with coatings, ferrites, and non-magnet metals.

- Observed failure mode: traceability dilution. Material from multiple collectors is blended before grade confirmation, obscuring provenance and mass balance.

- Observed failure mode: downstream gap. Separated rare earth salts are produced, but local alloying or magnet-making capacity is absent, leaving the recycling loop incomplete.

- Observed failure mode: heavy rare earth overstatement. Marketing emphasizes dysprosium and terbium recovery even when the actual end-of-life feed is dominated by low-Dy consumer or industrial magnet streams.

Why dysprosium and terbium remain the hard part

NdPr recovery is the visible part of the recycling story because neodymium-praseodymium dominates most permanent magnet applications. Dysprosium and terbium are harder. They are critical for high-temperature magnet performance, but end-of-life magnets often contain them in comparatively small amounts. Many consumer electronics magnets contain little or no meaningful heavy rare earth loading, and even in EV applications the Dy share is often modest. That means a large quantity of end-of-life material may still yield a limited amount of dysprosium or terbium, while the chemical separation burden remains high.

This is why recycling can support diversification without resolving near-term heavy rare earth risk. The most meaningful future feedstock for Dy and Tb sits in larger traction motors and wind turbine generators, and much of that stream becomes available only as assets are retired in larger numbers after 2030. Wind remains important because a single turbine can contain a substantial mass of permanent magnet material, but the timing of decommissioning, the magnet architecture, and the physical route from removal to controlled processing all determine real recoverability. In short, dysprosium recycling is technically possible, but operational scale is still emerging.

Compliance, jurisdiction, and refining geography

Geography matters twice in rare earth recycling: once at waste collection and again at refining. The EU has moved from general e-waste management toward more explicit strategic raw material thinking through the Critical Raw Materials Act, while WEEE rules continue to shape collection behavior. At the same time, China remains dominant across mining, separation, and magnet manufacturing, which means recycled oxide or salt produced elsewhere may still depend on Chinese refining or magnet conversion capacity unless domestic alloying and sintering lines are in place. That geographical dependence can leave a recycling project exposed even when collection is local.

Transboundary shipment rules, hazardous residue classification, and documentation quality also affect operational resilience. A recycler handling fluorescent phosphors, mixed electronics, and magnet scrap may face very different compliance burdens across those streams. Recent sector developments point toward more specialized facilities, more interest in domestic magnet loops, and stronger scrutiny of provenance claims. The pattern is clear: recycling is becoming more strategic, but the sector still rewards operational specificity over broad narrative.

A practical due-diligence frame for recycling claims

In practice, a recycling review often separates five questions. First, what exactly is the feedstock: production scrap, returned magnets, motors, turbines, or mixed e-waste? Second, how controlled is collection: contracted industrial scrap, municipal waste, or third-party aggregators? Third, which process route is used: direct magnet recycling, hydrometallurgy, or a hybrid? Fourth, how is traceability maintained across receipt, assay, separation, and sale? Fifth, what is the final product: reusable NdFeB alloy input, separated oxides, salts, or a lower-value mixed intermediate?

Across the global market, the most credible risk-mitigation models tend to be the least glamorous. Clean industrial scrap loops, degaussed hard-disk-drive magnets, and clearly identified manufacturing returns usually outperform diffuse consumer collection in both traceability and recovery quality. EV motor and wind turbine recycling remain strategically important because they represent future scale, yet their strongest contribution is likely to appear gradually as asset retirement volumes build. Recycling so sits as a genuine diversification tool within rare earth supply chains, especially for NdPr, while primary mining and separation still carry most of the burden for near-term dysprosium and terbium availability.

For Procyon Metals, the central analytical question is not whether recycling works in principle. It is where a given recycling claim sits on the spectrum between clean industrial-loop recovery and difficult mixed-waste recovery, and whether the evidence on feedstock control, process selection, traceability, and downstream conversion is strong enough to support the claim. Discussion of recycling claims and supply-chain due diligence in rare earths and magnet metals forms part of Procyon Metals’ ongoing work.