In rare earth magnets, disruption rarely begins with a headline about ore in the ground. The break usually appears further downstream: a separation circuit with limited heavy rare earth capability, a metal producer with inconsistent purity, a magnet plant qualified for samples but not serial production, or a document trail that stops at mine origin and says little about oxide, metal, alloy, and sintered magnet provenance. In family office and strategic metals review work, that is often the first important discovery: “non-China” can describe the mine while the highest-risk processing stages remain concentrated elsewhere.

Key takeaways

- The rare earth magnets supply chain is not a single market. Mining, separation, metalmaking, alloying, and magnet fabrication each have distinct concentration points and failure modes.

- NdPr provides the core magnetic performance in NdFeB magnets, while dysprosium and terbium protect coercivity in high-temperature and high-stress applications.

- China’s role becomes more concentrated downstream, especially in separation, heavy rare earth processing, alloy production, and finished magnet manufacturing.

- Demand signals differ by sector: EVs and wind create volume pressure, while robotics and defense increase sensitivity to high-specification Dy/Tb content and qualification traceability.

- Substitution and recycling exist, but both face practical limits in power density, thermal stability, collection, purity control, and industrial scale.

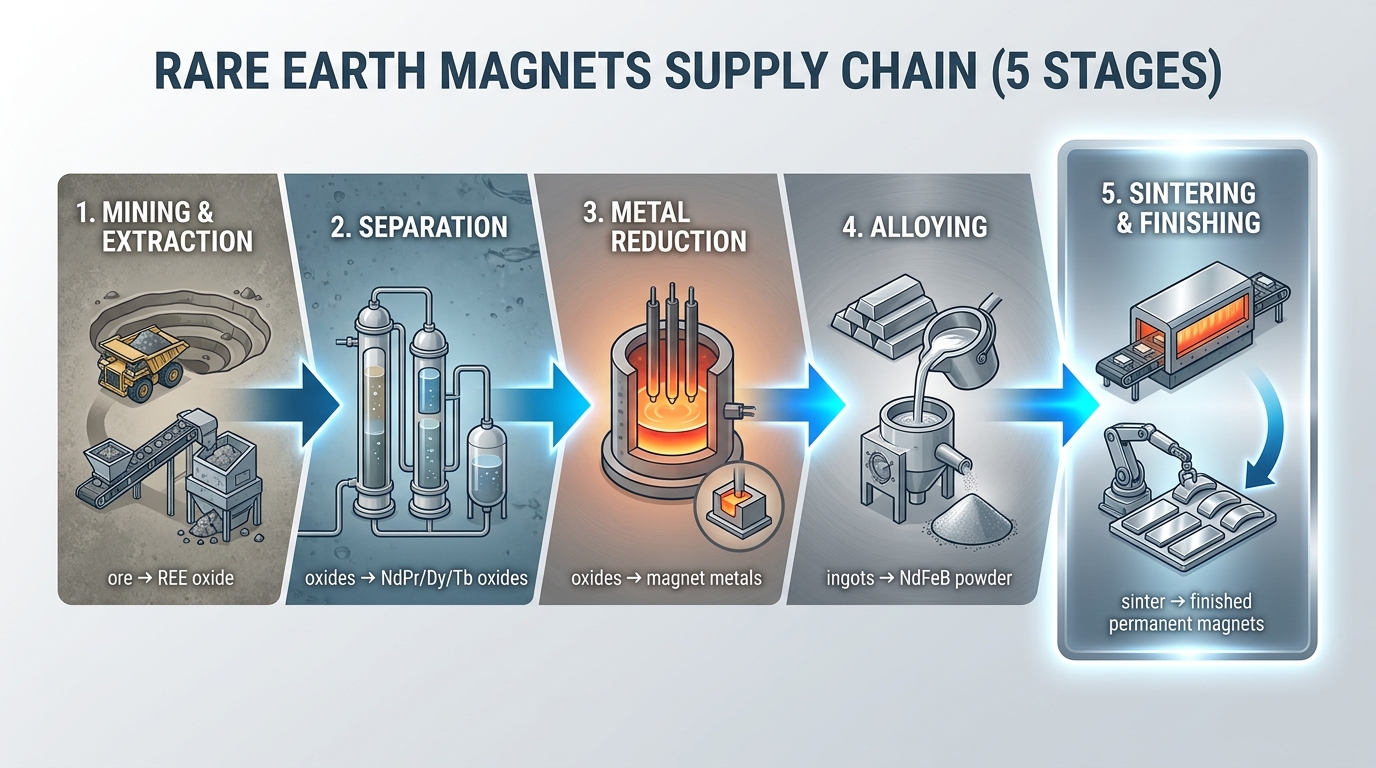

Mapping the chain from ore to permanent magnet

The chain begins with rare earth mineralisation, commonly bastnaesite or monazite, reported in TREO or REO terms. Mining and beneficiation produce a concentrate, but concentrate is only an intermediate. What matters for magnet metals is the contained distribution of light and heavy rare earths, impurity profile, radioactive handling obligations where relevant, and the route into a separation facility. A concentrate rich in total rare earths can still be strategically weak if its NdPr split is modest or if its heavy rare earth component is absent.

Separation is the pivotal stage. Solvent extraction trains divide mixed rare earth streams into individual oxides such as neodymium oxide, praseodymium oxide, dysprosium oxide, and terbium oxide. This is where many supply-chain maps become misleading. A mining project may sit in Australia, the United States, Africa, or Canada, while separation remains concentrated in China or in a small number of non-China facilities such as Lynas’ Malaysia operations. In practical reviews, separation capability often determines whether a project is truly relevant to the NdPr supply chain or simply relevant to upstream rare earth narrative.

From oxides, the chain moves to metal reduction, alloying, strip casting or related intermediate processing, powder production, pressing, sintering, machining, coating, and magnetisation. Each step narrows the field of capable operators. Magnet-grade metal requires controlled impurity levels, and ppm-level contamination can matter in downstream alloy and sintering performance. A recurring discovery in supplier assessments is that a project may present robust geology and a credible oxide story, yet still depend on an external party for alloying or magnet fabrication. For resilience analysis, mine-to-magnet continuity matters more than upstream abundance alone.

What NdPr, dysprosium, and terbium actually do

NdPr is the functional base of most high-performance neodymium-iron-boron magnets. Neodymium and praseodymium are commonly discussed together because they are often marketed and processed as a didymium stream before final optimisation. In simple terms, NdPr delivers the magnetic strength and energy density that make compact motors, generators, and actuators possible. That is why the NdPr supply chain sits at the centre of EV drivetrains, direct-drive wind systems, robotics actuators, industrial servomotors, and many aerospace applications.

Dysprosium and terbium are different. They are heavy rare earths, scarcer in economic concentrations and more difficult to separate. Their role is not to replace NdPr but to harden a magnet against heat and demagnetisation. In high-temperature operating windows, Dy and Tb preserve coercivity. This matters in traction motors, offshore installations, aerospace systems, and military platforms where thermal stress, vibration, and reliability requirements are more severe. The strategic issue is not only lower availability; it is the fact that Dy/Tb exposure often becomes visible late, when a magnet specification is already tied to an application that cannot easily tolerate redesign.

Analytical criteria used in a supply-chain review

A useful review framework separates geology from deliverability. The first criterion is chain-of-custody depth: mine, concentrate, separated oxide, metal, alloy, and finished magnet. The second is technical fit: whether the supplier can produce the relevant chemistry, grain structure, coating system, and thermal profile for the end use. The third is jurisdictional exposure, including export controls, licensing, environmental permitting, and customs documentation. The fourth is scale-up realism, because pilot lots and commercial continuity are not the same thing. The fifth is redundancy: whether more than one route exists for the critical step.

- Provenance evidence: certificate of analysis, country-of-origin records, conversion pathway, and where “mine-to-magnet” claims actually stop.

- Heavy rare earth visibility: declared Dy/Tb loading, ability to source heavy rare earth oxides or metals, and whether substitution assumptions are built into the magnet design.

- Processing bottlenecks: separation access, reduction know-how, alloy capability, and sintering qualification.

- Compliance burden: environmental permits, radioactive residue handling where relevant, export documentation, and sector-specific traceability expectations in automotive, aerospace, or defense channels.

- Ramp credibility: evidence that sample material, pilot output, and recurring production are coming from the same process route rather than a temporary workaround.

Demand signals that change the risk profile

Demand is not uniform across end markets. EVs are the largest visible source of volume pressure because a large share of traction motor architectures still relies on NdFeB magnets. Current industry coverage points to roughly 1-3 kg of NdFeB in many EV motor systems, while some system-level estimates run higher depending on architecture and component scope. At projected EV volumes, even the lower end of that range implies substantial NdPr draw. Recent arrangements between automotive groups and magnet makers such as GM and Noveon have been read in the market as evidence that downstream qualification capacity matters almost as much as raw material availability.

Wind power creates a different pattern. Offshore direct-drive turbines can require very large magnet loads per megawatt, making wind a major sink for NdFeB if deployment targets continue to rise. Robotics and high-performance motors add another layer because actuator precision and compactness can increase sensitivity to Dy/Tb content. Market commentary around humanoid robotics has drawn attention to magnet intensity per unit, even when aggregate volumes remain small relative to EVs and wind. Defense demand is smaller in tonnage but higher in criticality. Aircraft, drones, guidance systems, and high-temperature military electronics place more weight on qualified performance, thermal tolerance, and secure provenance than on simple bulk availability.

Why substitution and recycling remain constrained

Substitution is often presented as an easy release valve, but the engineering trade-off is usually severe. Ferrite, induction, or switched reluctance alternatives can remove or reduce rare earth dependence in some designs, yet they often give back power density, efficiency, size, or weight. In EVs, drones, robotics, and aerospace, those trade-offs can quickly become unacceptable. Samarium-cobalt occupies a real niche at high temperatures, but it is not a simple universal replacement for NdFeB and introduces its own material and manufacturing constraints.

Recycling is equally important and equally limited. Magnet scrap from manufacturing is easier to process than end-of-life material because chemistry is more predictable and contamination is lower. End-of-life recycling faces fragmented collection, coatings, mixed assemblies, uncertain Dy/Tb content, and the need to return material to magnet-grade quality. That is why recycling helps the system but does not yet remove dependence on primary supply. A practical observation from the field is that “recycled content” often improves feed flexibility without solving the hardest heavy rare earth bottlenecks.

Common failure modes observed in the rare earth magnets supply chain

- Upstream strength, downstream weakness: a credible mine with no assured separation, metal, or magnet route.

- Heavy rare earth blind spot: a magnet specification that quietly assumes future Dy/Tb access without showing the source.

- Pilot-to-production discontinuity: sample magnets qualified from one feedstock, then commercial lots produced from another.

- Traceability gap: origin claims at oxide level but limited transparency on metal reduction, alloying, or sintering.

- Policy shock: export licensing changes, sanctions risk, or customs scrutiny affecting intermediate forms rather than mined material.

- Application mismatch: a supplier able to make industrial magnets but not automotive, aerospace, or defense-grade material with the necessary documentation and consistency.

Observed risk-management configurations in the market

Several configurations have appeared as market participants try to reduce concentration risk. One is vertical integration from mine or mixed rare earth feed through separation and into magnet production. Another is partial regionalisation, with mining in one jurisdiction, separation in another, and final magnet production closer to end-use manufacturing. Current examples often cited in industry discussions include Lynas outside China in separation, MP Materials in the United States moving further downstream, and a range of North American and European groups seeking qualified non-China magnet routes. A separate pattern is the use of recycled magnet material to supplement virgin feed, particularly where manufacturing scrap is available. There is also visible work on reducing heavy rare earth loading through grain boundary diffusion and related processing improvements, although those approaches shift rather than eliminate technical dependence.

These configurations all carry trade-offs. Integrated chains improve visibility but take time to build. Regionalised chains can reduce geopolitical concentration while adding handoff complexity. Recycling improves material circularity but rarely resolves qualification and purity issues on its own. Lower-Dy or lower-Tb designs can reduce pressure on the scarcest inputs, yet they are application-specific and may not fit high-temperature duty cycles. From a resilience perspective, the most important distinction is between a chain that is merely diverse on paper and one that is operationally proven across oxide, metal, alloy, and finished magnet stages.

Related Procyon Metals resources

For broader context across critical materials, related reading includes the Critical Metals Pillar Guide and the Physical Strategic Metals Due Diligence Checklist. Further discussion with Procyon Metals on rare earth and magnet metals exposure commonly centres on provenance depth, heavy rare earth bottlenecks, and the difference between upstream optionality and downstream deliverability.