Rare-Earth-Free Motors and Low-Rare-Earth Designs: What the Engineering Reality Means for Strategic Metals Exposure

This explainer is written for family offices, strategic-metals investors, and supply-chain risk teams following the global motor market through an industrial lens rather than a headline lens. The central point is straightforward. Rare earth free motors are no longer theoretical, and low-rare-earth designs are becoming materially more important, but the substitution story is not a simple march from permanent magnets to magnet free motors. It is a segmented redesign of the drivetrain landscape, shaped by torque density, thermal stability, efficiency across duty cycles, manufacturing complexity, and upstream concentration in rare-earth processing and magnet fabrication.

That distinction matters because rare earth substitution is often presented as if one successful prototype can reset the entire demand picture for neodymium, praseodymium, or dysprosium. The operating evidence points elsewhere. In many end markets, especially compact high-performance electric traction, robotics, servo systems, and packaging-constrained industrial equipment, permanent magnet motors remain structurally advantaged. The debate is not whether alternatives exist. They do. The harder question is where the alternatives stay competitive once all losses, materials, controls, cooling demands, and reliability burdens are counted.

Why the substitution debate has intensified

The recent acceleration in rare-earth-free motor development is tied to a familiar industrial problem: concentrated midstream capacity. The bottleneck is not simply mine supply. It is separation, metal and alloy conversion, and magnet manufacturing. For traction systems built around NdFeB permanent magnets, supply resilience depends on a chain that runs from rare-earth oxides to alloying, sintering, machining, coating, and motor integration. A disruption in one part of that chain can travel quickly into automotive and industrial procurement.

Publicly disclosed programs from Astemo, Valeo, and ABB show how manufacturers are trying to reduce that dependence in different ways. Astemo stated in October 2025 that it had achieved 180 kW output from a rare-earth-free main drive motor based on synchronous reluctance principles, with practical application targeted around 2030. Valeo has promoted an electrically excited synchronous motor, or EESM, with hairpin stator architecture, presenting it as a zero-rare-earth design and citing a lower motor-level carbon footprint versus conventional permanent magnet synchronous motors. ABB has advanced ferrite-assisted synchronous reluctance systems for industrial use. These are not identical technologies. They solve different problems under different operating constraints.

Here is where the data becomes more useful than the headline. The market is not choosing between permanent magnet motors and one clean substitute. It is moving toward a layered architecture: high-NdPr motors in the most demanding applications, low-Dy magnets where heavy-rare-earth thrift is feasible, ferrite-assisted designs where size and efficiency penalties are manageable, and genuinely magnet-free machines where system-level trade-offs remain acceptable.

What “rare-earth-free” actually means in motor design

The phrase rare earth free motors covers several very different machine topologies. That matters because performance comparisons can become misleading when one architecture is judged only on peak power rather than on full duty-cycle behavior, thermal margin, or packaging.

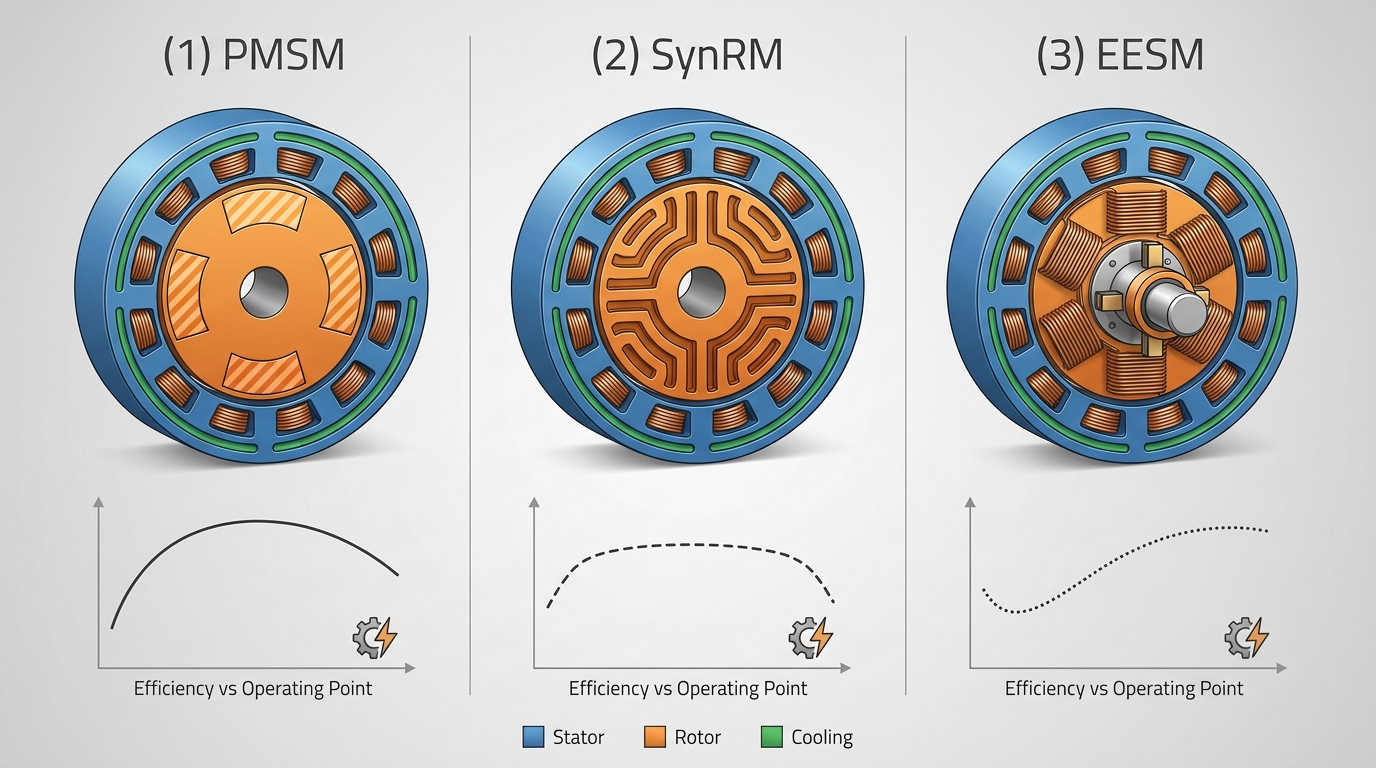

- Induction motors use a squirrel-cage rotor, typically aluminum or copper, and generate torque through induced rotor currents. They contain no permanent magnets.

- Synchronous reluctance motors, or SynRM, rely on rotor saliency and magnetic reluctance differences rather than rotor magnets. They are magnet free by design.

- Electrically excited synchronous motors, or EESM, replace permanent magnets with field windings energized electrically. They are magnet free, but not excitation free.

- Ferrite-assisted motors use ferrite magnets instead of rare-earth magnets. They are not magnet free motors, but they are low-cost and non-rare-earth in the rotor magnet system.

- Low-rare-earth magnets usually refer to NdFeB systems engineered to reduce heavy rare earth content, especially dysprosium, or to partially substitute more abundant rare earths such as cerium or lanthanum in less demanding applications.

| Architecture | Rare-earth exposure | Main strength | Main limitation | Typical fit |

|---|---|---|---|---|

| Permanent magnet synchronous motor | High to moderate, depending on magnet formulation | Torque density, compactness, high efficiency | Rare-earth and magnet supply-chain dependence | EV traction, robotics, servo drives, compact industrial systems |

| Induction motor | None in rotor drive magnet system | Mature, robust, no permanent magnets | Rotor losses, cooling burden, lower efficiency in many duty cycles | Industrial drives, some EV platforms, pumps and compressors |

| SynRM / ferrite-assisted SynRM | None to low | No NdPr requirement or reduced magnet intensity | Control complexity, lower torque density, acoustic and thermal challenges | Industrial systems, selected hybrid and EV platforms |

| EESM | None in main rotor magnet system | Eliminates permanent magnets, tunable field strength | Field excitation losses, added copper and rotor complexity | Selected automotive and industrial applications |

Why permanent magnet motors remain difficult to replace

Permanent magnet motors remain hard to displace for a simple physical reason: they place a strong magnetic field in the rotor without continuous electrical excitation. That eliminates field-current losses and supports high torque density in a compact envelope. The result is not just better headline efficiency. It is easier packaging, lower rotor heating, simpler cooling loads at equivalent output, and strong performance across a wide operating map.

General engineering literature, echoed in the research brief, places ferrite magnetic energy density at roughly 200 to 250 kJ/m³, compared with around 240 to 400 kJ/m³ for neodymium-based magnets depending on grade. That gap is one reason ferrite alternatives often need a larger magnetic circuit to reach similar torque. More volume means more mass, tighter packaging pressure, and frequently a wider penalty across rotor design, cooling jacket geometry, and vehicle integration. In compact traction systems, the penalty compounds quickly.

The substitution debate is often framed as magnets versus no magnets. The engineering reality is harsher: losses never disappear; they migrate. A motor can remove NdPr from the rotor and still become more metal-intensive elsewhere, with more copper in field windings, more electrical steel in the magnetic path, more inverter sophistication, and more aggressive cooling hardware. That does not invalidate substitution. It simply defines its cost.

Heavy rare earths deepen the picture. Dysprosium is often added to improve coercivity and protect magnet performance at elevated temperature, but that comes with supply-chain exposure and a magnet-property trade-off of its own. Low-Dy or Dy-thrift magnet strategies therefore matter enormously. They do not create rare earth free motors, but they reduce one of the most operationally sensitive inputs while preserving much of the permanent magnet architecture that OEMs already know how to industrialize.

The commercially credible rare-earth-free pathways

Induction motors: the mature magnet-free benchmark

Induction motors are the most established rare-earth-free alternative. The rotor contains no permanent magnets, and the manufacturing base is well understood globally. That maturity is the attraction. The limitation is equally familiar: rotor current generates heat. Those I²R losses reduce efficiency, especially outside optimized operating points, and they impose a cooling burden that becomes more consequential in compact vehicle traction. Induction machines remain credible where robustness and magnet independence rank above absolute torque density, but they rarely erase the packaging advantage of permanent magnet motors.

Synchronous reluctance motors: credible, but highly geometry-dependent

SynRM architectures generate torque from the rotor’s tendency to align along the path of least magnetic reluctance. In plain terms, the rotor geometry does much of the work. That sounds elegant, and in many industrial settings it is. But the geometry also makes the design sensitive to rotor lamination quality, control strategy, vibration behavior, and partial-load performance. Public statements from Astemo indicate that a rare-earth-free SynRM-based main drive motor has reached 180 kW output, with practical application envisioned around 2030. The milestone is significant because it demonstrates that magnet-free automotive traction is not confined to niche laboratory work. The constraint is that scaling from demonstrated output to broad, mass-market deployment is a manufacturing and system-integration challenge, not just a physics exercise.

Ferrite-assisted SynRM designs improve the picture by adding low-cost non-rare-earth magnets to the rotor. ABB’s industrial work is relevant here. Ferrite assistance can raise efficiency and torque density over a pure SynRM, but the magnet strength remains lower than NdFeB, so the architecture still relies on careful control and often accepts a size or mass trade-off. This is one of the more important nuances in the market. Some “rare-earth-free” narratives are actually “rare-earth-free but not magnet-free,” and that distinction directly affects bill-of-material resilience.

Electrically excited synchronous motors: magnet-free, copper-heavier, control-heavier

EESM designs eliminate permanent magnets by energizing a rotor field winding. Valeo has presented this route with a hairpin stator, claiming a lower carbon footprint at motor level versus conventional permanent magnet machines and higher power density versus earlier EESM generations. The engineering logic is sound. Hairpin stators can raise slot fill and improve heat management in the stator. Even so, the machine still needs field excitation. That means electrical energy is continuously allocated to maintaining the rotor field, and the machine inherits extra copper demand, rotor winding complexity, and potential reliability sensitivities around excitation hardware, insulation systems, and thermal management.

This is the second critical insight. Permanent magnets remain difficult to replace not because alternatives are absent, but because permanent magnet machines compress torque, efficiency, and packaging into one architecture with very few moving trade-offs. EESM and SynRM can be highly effective. They simply move the compromise elsewhere.

Low-rare-earth designs may matter more than “magnet-free” headlines

The most underestimated resilience pathway in the market is not total magnet elimination. It is material thrift inside the permanent magnet family. Low rare earth magnets can take several forms: reduced dysprosium content through better grain-boundary engineering, better cooling strategies that lower rotor temperature exposure, selective use of terbium or alternative microstructural treatments in demanding zones, and partial substitution with more abundant rare earths in applications with looser thermal or torque requirements.

This matters because dysprosium exposure is not the same as NdPr exposure. A motor program that materially lowers heavy-rare-earth intensity can still preserve the compactness and efficiency of a permanent magnet motor while improving supply resilience. For strategic-metals analysis, that is not a side note. It is a separate demand outcome. A world with more low-Dy permanent magnet motors is not a world without rare-earth demand. It is a world with a different composition of rare-earth demand and a different sensitivity to thermal-grade magnet capacity.

Some formulations also explore partial cerium or lanthanum substitution. These routes can lower cost pressure and diversify feedstock usage, but they generally carry performance penalties that confine them to less demanding duty cycles. Again, the pattern is consistent. Rare earth substitution is real, but it is segmented. High-end traction, precision servos, and compact direct-drive systems are not governed by the same trade-offs as auxiliary pumps or standard industrial drives.

Where substitution works, and where it becomes expensive insurance

Substitution works best when the operating envelope is narrow, the packaging envelope is forgiving, and the system can tolerate either more mass, more copper, more control sophistication, or somewhat lower partial-load efficiency. That makes industrial drives, commercial vehicles on predictable duty cycles, and some hybrid architectures the leading candidates. In these settings, SynRM, ferrite-assisted machines, and selected EESM configurations can reduce rare-earth exposure without breaking the application.

Hybrid electric vehicles are a particularly important middle ground. The electric machine is not always asked to deliver the entire propulsion burden, which eases some efficiency and packaging constraints. Ferrite-based designs and reluctance-based systems can therefore make more sense than they do in battery-electric platforms that rely on electric traction continuously. Commercial vehicles present another case where duty-cycle predictability can support alternative topologies, especially when routing, load profiles, and cooling systems are already tightly engineered.

The hardest territory remains the compact, efficiency-sensitive, thermally demanding application set. Premium battery-electric platforms, precision robotics, servo drives, drones, and other systems where every kilogram and every cubic centimeter counts continue to favor permanent magnet motors. In those systems, rare-earth-free designs can function as expensive insurance against supply disruption. They are technically valid, but the premium is paid through packaging penalty, lower efficiency at key duty points, more complicated control, or more difficult thermal management. That is not a universal rejection of substitution. It is a reminder that substitution has an industrial price, even when headline material exposure declines.

What this means for rare-earth demand resilience globally

The strongest conclusion from the current evidence is that rare-earth-free motors reduce demand concentration in selected applications, but they do not eliminate magnet metal demand. Even if magnet-free traction gains meaningful share over time, several sources of residual demand remain: permanent magnet motors in premium or packaging-constrained platforms, auxiliary vehicle systems, robotics, industrial servos, wind systems, compressors, and a wide range of electronic and electromechanical assemblies that still value NdFeB performance.

There is also a supply-chain substitution effect. When a manufacturer moves away from permanent magnets, the dependency does not vanish. It shifts toward copper, electrical steel, ferrite supply, power electronics, software calibration, and specialized manufacturing tolerances. In some cases, the rare-earth bottleneck is exchanged for a different bottleneck in conductor quality, insulation endurance, or inverter capability. From a resilience standpoint, that can still be rational. From a demand-destruction standpoint, it is much less dramatic than the headline “magnet free” suggests.

Widely cited industry estimates summarized in the research brief place China at roughly 70% of global rare-earth processing and about 60% of primary production. Those figures help explain the urgency behind substitution programs, but they do not automatically translate into a collapse of rare-earth dependence. The practical market outcome is more likely a bifurcation. One part of the motor market leans harder into rare-earth-free or low-rare-earth architectures for resilience. Another part continues to pay for permanent magnet performance because the alternatives remain too large, too lossy, or too operationally complex.

This is the third insight worth isolating. The relevant question is not whether rare earth free motors exist. The relevant question is how much rare-earth intensity can be removed before the application starts paying for that resilience somewhere else in the system. In many sectors, the answer is “some, but not all.” That is why permanent magnet demand can remain resilient even as substitution headlines multiply.

Implementation, maintenance, and compliance constraints

Motor substitution is not only a materials question. It is a manufacturing and operations question. SynRM designs depend heavily on rotor lamination precision, electromagnetic modeling, inverter tuning, and noise-vibration-harshness control. EESM platforms add rotor winding and excitation complexity, which can introduce different reliability modes than a permanent magnet rotor. Induction motors place more attention on rotor heating and cooling design. None of these constraints is fatal. All of them affect industrialization speed.

Compliance also shifts. Rare-earth-free systems can ease concerns around critical minerals exposure and, in some jurisdictions, simplify end-of-life handling by removing the need for permanent magnet recovery. At the same time, higher copper content, different insulation systems, and more demanding thermal cycles raise separate questions for lifecycle qualification and maintenance. A rare-earth-free motor may reduce one class of supply-chain risk while introducing a more exacting reliability validation program on another axis.

This connects directly to cost. Public announcements emphasize technical achievement, but manufacturing economics are less transparent. Tooling, rotor complexity, winding processes, control software calibration, and validation time all influence whether a rare-earth-free solution is a broad market answer or a selective hedge. In practice, some motor architectures will remain highly application-specific for years because qualification effort is as real a barrier as materials availability.

Observed market configurations rather than a single end state

The most realistic global picture is not total replacement, but coexistence. One observed configuration is the performance-led platform that keeps permanent magnets and reduces heavy-rare-earth intensity through material optimization. Another is the resilience-led platform that accepts a magnet-free or ferrite-assisted design where packaging and duty cycle permit. A third is the mixed portfolio, common in large OEMs and industrial groups, where different motor topologies are assigned to different products rather than imposed across the entire range.

That portfolio logic is exactly why rare-earth demand resilience can persist even while substitution advances. The motor market is too heterogeneous for a single topology to dominate every application. The companies most vocal about substitution are often the same companies maintaining multiple architecture pathways at once. That is not inconsistency. It is industrial realism.

FAQ: Can EV motors avoid rare earths

Yes, some EV motors can avoid rare earths. Induction motors, synchronous reluctance motors, and electrically excited synchronous motors are all credible pathways for eliminating rare-earth permanent magnets from the main traction motor. Publicly discussed programs from Astemo and Valeo demonstrate that automotive-grade development is active and technically serious. The limit is not basic feasibility. The limit is application fit. Once packaging, efficiency over real drive cycles, cooling burden, mass, and manufacturing complexity are factored in, rare-earth-free traction becomes more compelling in some vehicle segments than in others. The conclusion is selective viability, not universal replacement.

FAQ: Do rare-earth-free motors eliminate magnet metal demand

No. Rare-earth-free motors do not eliminate magnet metal demand at system level or market level. First, many vehicles and industrial systems still retain permanent magnets in auxiliary motors, sensors, actuators, and non-traction subsystems. Second, ferrite-assisted machines still use magnets, even if they avoid rare earths. Third, many high-performance applications continue to favor permanent magnet motors because torque density and compactness remain decisive. The demand effect is therefore dilution and redistribution, not removal. For NdPr and dysprosium analysis, that distinction is fundamental.

Note on Procyon methodology Procyon Metals cross-references trade-policy signals, including export-control and administrative notices such as MOFCOM actions when relevant, with disclosed OEM engineering claims and the end-use performance specifications that actually govern adoption. That approach matters because market narratives around rare earth substitution often outrun the thermal, packaging, and reliability limits embedded in the final application.

Conclusion

Rare earth free motors are real, low-rare-earth designs are becoming more sophisticated, and the motor market is clearly diversifying. But diversification is not the same as displacement. In the applications that matter most for torque density, compact packaging, and efficiency across demanding duty cycles, permanent magnet motors remain unusually hard to replace, while low-Dy and other thrift strategies may prove more consequential than magnet-free headlines suggest.

For family offices, strategic-metals investors, and industrial counterparties mapping continuity risk rather than chasing simplistic substitution narratives, the operative framework is exposure redistribution across motor architectures, materials, and operating constraints. Procyon Metals is available to discuss rare earth exposure scenarios across rare earth free motors, magnet free motors, permanent magnet motors, and low rare earth magnets, supported by active monitoring of weak signals that will define the next phase.