In rare earth supply reviews, the first operational surprise is often how little the headline NdPr story explains about real downstream exposure. Magnet metals dominate public coverage, yet production teams, specialty materials buyers, and strategic metals research functions regularly encounter a different constraint set in yttrium, europium, and gadolinium. These elements sit in phosphors, ceramics, medical imaging inputs, nuclear materials, microwave electronics, and defense-adjacent systems. They are usually not mined for their own sake. They are recovered, separated, purified, and qualified as part of a much more complicated basket logic.

- NdPr explains magnet demand, but it does not explain the full rare earth risk picture; yttrium, europium, and gadolinium follow different end-use and refining pathways.

- Supply risk is shaped less by ore abundance alone than by by-product economics, separation capacity, product purity, and jurisdictional concentration.

- Yttrium matters in phosphor host materials and advanced ceramics; europium remains tightly linked to red phosphors and optical systems; gadolinium crosses into MRI contrast agents, neutron absorption, and specialty electronics.

- Export-control sensitivity often appears at the downstream material or end-use level, not only at the mixed rare earth concentrate or oxide level.

- Observed monitoring signals include basket chemistry, non-Chinese separation progress, qualification status, document completeness, and exposure to China-linked refining routes.

Why NdPr is not the whole rare earth story

The magnet narrative is real, but it is incomplete. Neodymium and praseodymium support electric motors, wind turbines, and many industrial drives, so they naturally attract the most attention. The analytical blind spot appears when that volume story is treated as a proxy for all rare earth risk. Yttrium, europium, and gadolinium belong to smaller, thinner, more application-specific markets where substitution can be limited and separation capability matters as much as mine output.

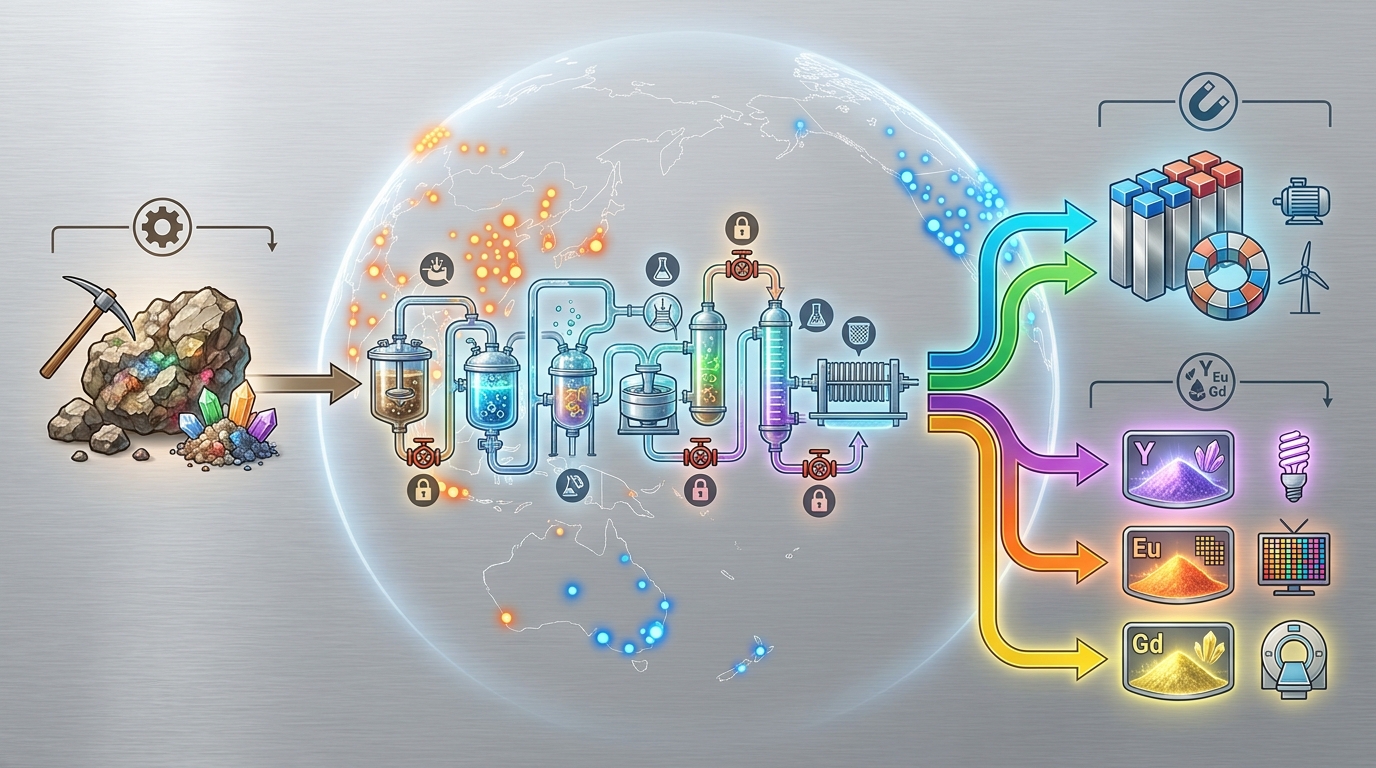

A recurring discovery in supplier assessments is that nominal mine capacity says very little about separated oxide availability. The relevant question is not simply whether ore exists, but whether the operator can recover a given element from the basket, refine it to the needed purity, and move it through a compliant route into a specialized end use. This is where overlooked rare earth elements become operationally important. A production line may not fail because rare earth ore is absent; it may fail because a niche oxide, dopant, or compound is unavailable in qualified form.

Analytical perimeter for a watchlist review

A practical review of yttrium supply chain exposure, europium rare earth availability, and gadolinium applications usually covers a small set of recurring criteria. The framework is descriptive rather than predictive, but it tends to separate robust supply chains from fragile ones.

- Basket chemistry: whether the host ore or concentrate actually carries meaningful yttrium, europium, or gadolinium content.

- Recovery route: whether the element is realistically recovered or simply present in trace amounts that are not separated commercially.

- Refining position: where solvent extraction, separation, oxide production, or downstream compound preparation takes place.

- Product form: mixed concentrate, carbonate, oxide, metal, doped phosphor, contrast-agent precursor, or engineered ceramic input.

- Qualification burden: whether the end market requires pharmaceutical, nuclear, defense, or electronics-grade validation.

- Jurisdictional exposure: reliance on China-based mining, separation, export licensing, or transshipment routes.

- Failure modes: by-product cutbacks, purity drift, customs holds, end-use screening, or loss of downstream qualification.

Yttrium: phosphor host, ceramic stabilizer, and a concentrated refining story

Yttrium rarely attracts the attention given to magnet materials, yet it remains central to two important product families. The first is phosphor chemistry, where yttrium oxide often acts as a host lattice for rare earth dopants in display and lighting materials. The second is advanced ceramics, especially yttria-stabilized zirconia and related high-temperature applications. In practice, this means yttrium touches both electronics and industrial materials, with very different qualification pathways.

The supply side is highly concentrated. Bayan Obo in Inner Mongolia, operated by China Northern Rare Earth Group, remains the most important reference point in any global map. It is the world’s largest rare earth deposit and produces yttrium as a by-product of iron ore and rare earth extraction. Reported rare earth concentrate capacity is in the range of 120,000 to 150,000 tonnes annually, with yttrium accounting for roughly 3 to 5 percent of the rare earth basket. Outside China, Mountain Pass in California produces about 40,000 tonnes of rare earth concentrate annually, with estimated yttrium recovery of roughly 1,200 to 1,500 tonnes per year, contingent on processing capacity and the broader basket economics. Lynas, with mining in Western Australia and processing in Kuantan, Malaysia, is another relevant non-Chinese node, with annual rare earth production around 11,000 tonnes and estimated yttrium recovery in the range of 300 to 400 tonnes.

The main failure mode in yttrium is not geological scarcity in isolation; it is dependence on the wider rare earth basket. When operators optimize around higher-profile outputs, yttrium recovery can become secondary. Another observed issue is that end users may speak about “yttrium” as if oxide, ceramic powder, and phosphor precursor are interchangeable forms. They are not. Purity, particle behavior, and downstream processing history can matter as much as origin. In periods of tighter trade scrutiny, document packages such as certificates of analysis, origin statements, safety documentation, customs classification, and end-use paperwork move from back-office detail to central risk factor.

Europium: a niche element with low substitution tolerance

Europium is one of the most easily overlooked rare earth elements because its market is small, specialized, and tied to functions that disappear inside a finished product. Its best-known role is as a red phosphor activator, particularly in europium-doped yttrium systems used in display technologies and optical materials. In plain terms, it is one of the reasons the red channel in phosphor-based systems works as intended.

Operationally, europium is difficult because the market is thin and the element is present in very low concentrations in many deposits. A second discovery from fieldwork and supplier mapping is that “available in the ore” often overstates what can be produced at separated, saleable quality. Europium tends to depend on a narrow band of processors with the technical willingness to recover and refine it. That makes the europium rare earth chain vulnerable to outages, maintenance events, and policy moves that would look minor in a larger commodity but become material in a niche material.

China remains the dominant center of gravity here as well, with Bayan Obo and related Inner Mongolian operations feeding state-owned and licensed private refining systems. Mountain Pass and Lynas matter as alternative nodes, but non-Chinese scale remains limited relative to China’s separation infrastructure. The practical implication is that europium availability often reflects processing commitment rather than mining headlines. A mine can be operating, a concentrate can be flowing, and yet downstream users can still experience tightness in a specific europium-bearing product.

For export-control analysis, europium also deserves special attention because the control question may arise through the end use. Optical systems, detection equipment, specialty phosphors, and defense-adjacent electronics can trigger scrutiny even when the underlying oxide does not appear to be the only regulated item. That downstream sensitivity is one reason europium belongs on a rare earth watchlist even if it never becomes a volume story comparable to NdPr.

Gadolinium: medical imaging, neutron absorption, and dual-use complexity

Gadolinium sits in a broader application set than europium, but the supply chain is not necessarily simpler. The most visible use is in gadolinium-based contrast agents for MRI imaging, where the element’s magnetic behavior makes it valuable in diagnostic workflows. It also appears in nuclear contexts because of its strong neutron absorption properties, and in specialty electronics such as garnets and microwave materials. Defense relevance enters through sensors, electronics, and systems where these properties are not easily replicated without performance trade-offs.

The key analytical feature of gadolinium is that end-market diversity creates multiple qualification environments. Medical applications bring pharmaceutical and regulatory expectations. Nuclear applications add strict material control and documentation requirements. Electronics and defense pathways can add dual-use review, product testing, and provenance scrutiny. A supplier may be acceptable for one industrial oxide application and unusable for a medical or nuclear pathway because the documentation trail, impurity profile, or validation history is not aligned.

In practice, gadolinium failure modes often include purity drift, inability to maintain application-specific specifications, and delays related to compliance rather than simple tonnage shortages. This is one reason gadolinium applications deserve separate treatment in strategic materials analysis. A seemingly modest disruption at the separation stage can propagate into hospitals, reactor supply chains, or specialist electronics manufacturing in ways that are disproportionate to the element’s public profile.

Export-control relevance and the role of China-linked processing

Export-control discussions around rare earths are often simplified into a binary question: restricted or unrestricted. The operational reality is more layered. China’s position in mining and especially in separation gives it leverage even when formal bans are absent. The practical chokepoint often sits in licensed exports, quota-like administrative behavior, or prioritization of domestic downstream users during periods of tighter supply. For yttrium, europium, and gadolinium, this matters because the value often resides in a high-purity or application-specific compound rather than a generic mixed product.

A third discovery from trade and supplier mapping is that compliance risk can attach to the route as much as to the origin. Material mined in one jurisdiction may still travel through China-linked separation, Malaysia-based processing, or downstream finishing elsewhere before reaching the final customer. Mountain Pass in the United States and Lynas in Australia and Malaysia have become important reference points in discussions about diversification, but the degree of independence depends on exactly which step is under review: concentrate production, separation, metallization, compound preparation, or final component manufacture.

Observed management patterns in the market

Across specialty materials markets, several risk-management patterns appear repeatedly. Some groups qualify more than one geographic source for the same oxide or downstream compound. Others reduce exposure by tracking not only miners but also separators and compound makers, since the bottleneck often emerges after the mine gate. Recycling and reclamation occasionally appear in phosphors and specialty ceramics, though they rarely eliminate dependence on primary supply. In high-consequence applications, stockholding, approved-vendor structures, and tighter document control are common features of the operating model.

These patterns also show why overlooked rare earth elements are not equally “investable” or equally scalable. Some belong on a watchlist because disruption would matter, not because the addressable market is broad. That distinction is especially relevant for family offices, strategic metals mandates, and private wealth research teams trying to separate narrative value from actual supply-chain significance.

What belongs on the watchlist

The case for tracking yttrium, europium, and gadolinium is straightforward: they reveal the parts of the rare earth system that the NdPr narrative leaves out. Yttrium highlights by-product dependence and the importance of phosphor and ceramic supply chains. Europium highlights low substitution tolerance in a very thin market. Gadolinium highlights how a single element can bridge medicine, nuclear systems, electronics, and defense screening. Together, they show that rare earth resilience is shaped by refining capability, qualification status, compliance burden, and route dependency at least as much as by mine tonnage.

That is why these materials remain relevant entries on a rare earth watchlist even when they are not the largest-volume names in the sector. Procyon’s strategic metals watchlist discussion commonly examines these dependencies alongside magnet materials, separation bottlenecks, and export-control developments when mapping global supply risk.