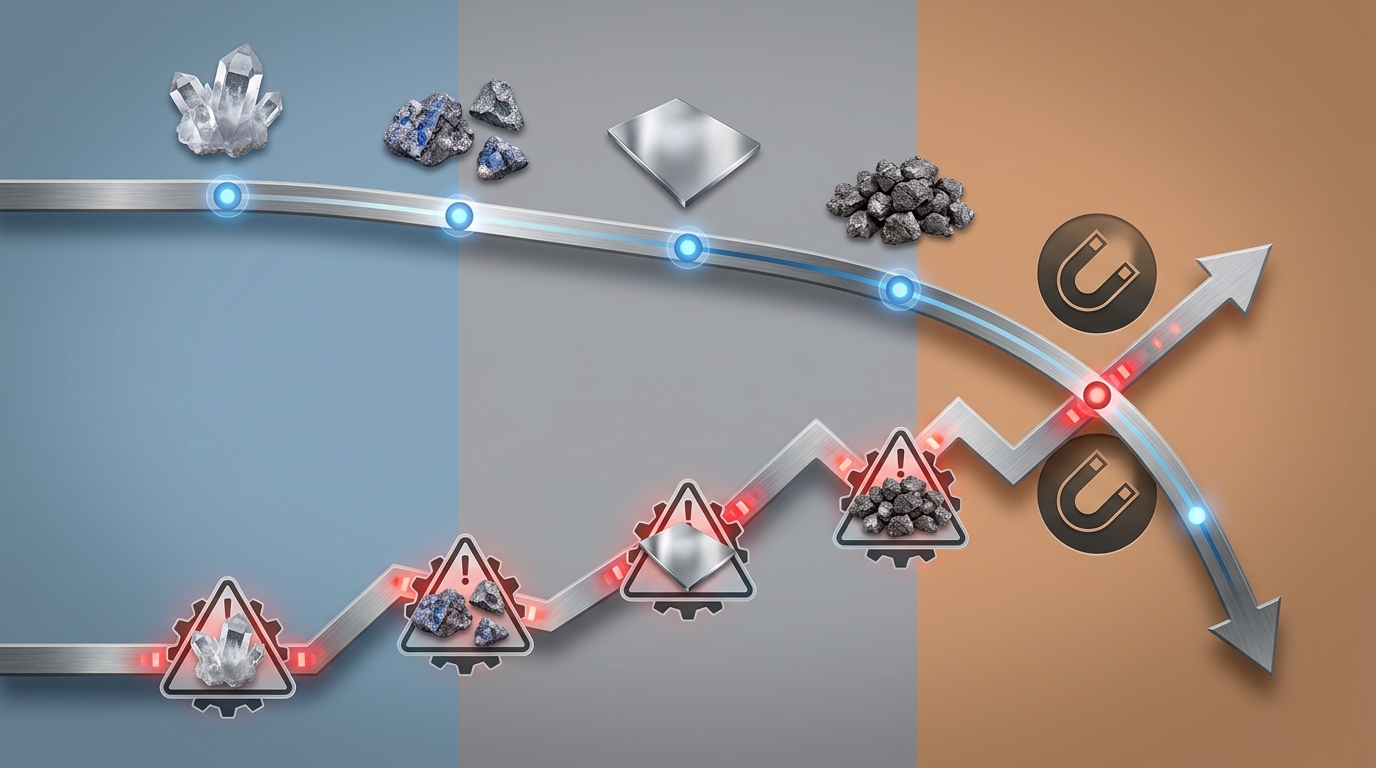

Soft or falling spot prices in lithium, cobalt, nickel, manganese, and selected rare earth products have often been read as evidence that scarcity has eased. Operational reviews across recent disruptions showed a more complicated pattern. Material could be abundant at the ore or concentrate stage while availability at the refined, qualified, or exportable stage remained tight. In the market background behind this brief, lithium was described as down roughly 75% during 2023, while other battery materials also weakened sharply from recent highs. At the same time, export-control risk, refining concentration, project delays, and strategic dependence on a small number of jurisdictions became more visible rather than less.

Key takeaways

- Spot weakness and supply security measure different things; price can soften while deliverability deteriorates.

- Refining concentration is often the governing bottleneck, especially where conversion capacity is concentrated in one country or a small number of processors.

- By-product metals behave differently from primary commodities because output depends on another metal’s production economics.

- Export controls, licensing, and customs enforcement can restrict supply even when global mine production appears ample.

- Project pipelines often slow during price weakness, creating future tightness that is not visible in the prompt market.

Analytical scope: where supply risk actually sits

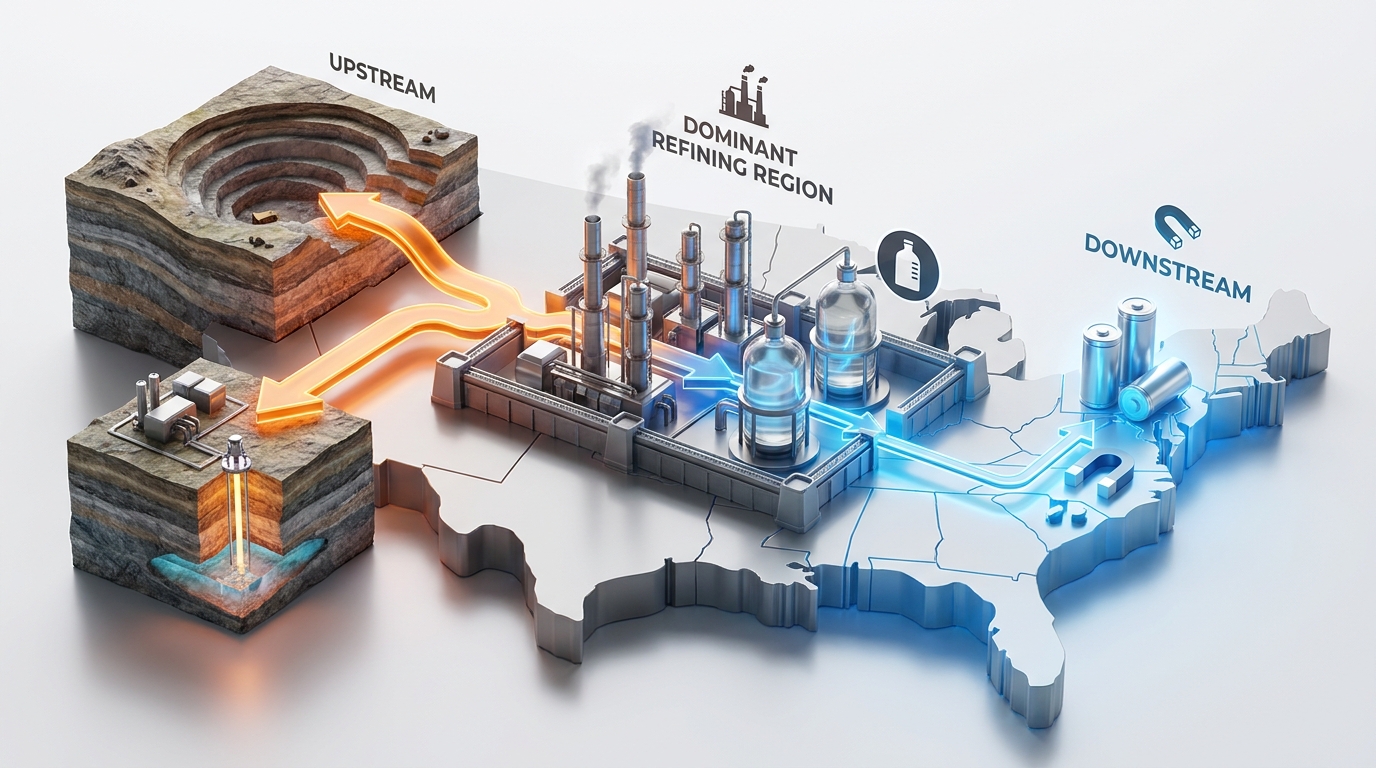

Critical minerals supply risk rarely sits in one place. A useful assessment separates the chain into four layers: resource extraction, intermediate processing, final refining, and market access. The distinction matters because the apparent surplus can sit upstream while the actual bottleneck sits downstream. Lithium quoted in LCE, or lithium carbonate equivalent, can look plentiful on paper even when battery-grade hydroxide conversion is constrained. Rare earth projects reported in TREO, or total rare earth oxide, can appear large while the magnet-relevant fractions such as NdPr, dysprosium, or terbium remain limited. In practice, the chain fails at the narrowest qualified stage, not at the most visible headline stage.

- Physical form: ore, concentrate, mixed carbonate, oxide, metal, alloy, magnet, or chemical precursor.

- Refining route: the number of steps between mine output and usable material, including solvent extraction, separation, calcination, or precursor synthesis.

- Jurisdictional concentration: where mining, refining, and export clearance are concentrated.

- Qualification status: whether the material is merely produced or actually approved for industrial use at required impurity levels, often measured in ppm.

- Documentary friction: certificate of origin, assay, safety data, chain-of-custody records, export licensing scope, and HS code alignment.

Can supply risk rise while prices fall?

Yes, and recent market behavior made that contrast unusually clear. Spot prices respond quickly to visible inventory, temporary oversupply, destocking, and financial positioning. Supply risk responds to a different set of variables: concentration of refining, fragility of trade routes, permitting delays, qualification cycles, and policy intervention. The result is a recurring disconnect. A large wave of spodumene, laterite, or mixed concentrate can depress the headline market while the useful product form remains exposed. One discovery repeated across battery materials and rare earths was that “available” often meant available in the wrong location, wrong chemical form, or wrong specification.

That distinction becomes sharper in concentrated markets. A seaborne cargo moving from Australia to China, a rare earth intermediate moving from Myanmar into Chinese separation plants, or cobalt-bearing feed moving from the Democratic Republic of Congo into Chinese or European refineries can all exist physically while still being vulnerable to licensing, customs inspection, plant outages, reagent shortages, or political decisions. None of those frictions is visible in a spot chart alone.

- Observed failure mode: surplus upstream, bottleneck downstream.

- Observed failure mode: material produced, but not qualified for the end-use application.

- Observed failure mode: exportable volume restricted by licensing rather than geology.

- Observed failure mode: single-country refining exposure creating high correlation across suppliers.

Refining concentration: the bottleneck that survives price weakness

Refining concentration is one of the most important reasons why low prices do not automatically solve critical minerals supply risk. In lithium, additional ore from Australia, Argentina, or Chile does not by itself create secure access to battery-grade chemicals. The conversion stage remains specialized, capital intensive, and geographically concentrated. Similar logic applies to cobalt sulfate, nickel Class 1 products, spherical graphite, and separated rare earth oxides. A market can be long raw material and short refined product at the same time.

Rare earths show the issue in its clearest form. Mining and concentration are only the opening steps. Separation into individual oxides, then conversion into metals, alloys, and magnets, creates several additional choke points. Even when non-Chinese rare earth projects report meaningful TREO, the relevant question is often whether separated NdPr oxide, dysprosium oxide, or terbium oxide can move through a qualified downstream chain. In practice, concentration in separation and magnet making has mattered as much as concentration in mining. A notable discovery in market reviews was that many “alternative” supply stories still depended on the same small cluster of downstream processors.

By-product dependency: why adjacent metals can tighten unexpectedly

By-product metals behave differently because their supply is tied to the economics of another commodity. Cobalt is largely associated with copper and nickel production. Indium depends heavily on zinc refining. Tellurium and selenium depend on copper anode slimes. Gallium can be linked to alumina processing, and germanium to zinc and coal-related streams. In these cases, a weak spot market for the by-product does not necessarily determine output. The controlling variable is often whether the host metal continues to be mined and processed at sufficient intensity.

This creates a recurring analytical trap. A low cobalt price can coincide with tight future cobalt availability if copper or nickel expansion slows. A soft dysprosium market can still be strategically tight if the light rare earth circuit that carries it is curtailed. The same logic applies when geology fixes the output ratio. Rare earth deposits do not respond neatly to demand for a single element; the basket composition comes from the ore body. As a result, markets for NdPr, Dy, and Tb can diverge from the headline tone of TREO or mixed rare earth concentrate. Strategic scarcity often hides inside the basket.

Export controls and regulatory scarcity

Export controls create another channel through which supply risk can rise independently of price. In rare earths and adjacent materials, policy actions can target ore, intermediates, processing equipment, chemical inputs, or finished products such as magnets. The practical effect is to shift the relevant question from “How much exists globally?” to “What can legally leave the jurisdiction, in what form, and under which documentation?” This distinction has become more important as governments increasingly treat critical minerals as strategic industrial inputs rather than ordinary commodities.

China remains central to this discussion because of its role in rare earth separation, magnet production, and several battery-material processing chains. Indonesia illustrates a parallel dynamic through nickel policy, where domestic-processing requirements have shaped global flows regardless of ore abundance. Myanmar matters in heavy rare earth feed, the Democratic Republic of Congo in cobalt-bearing material, and graphite markets remain sensitive to processing concentration and trade restrictions. A recurring discovery in customs and compliance reviews is that the constraint sometimes sits in classification, licensing scope, or proof of origin rather than physical shortage. Cargo can exist, and still not move.

Project delays and the gap between strategic need and actual capacity

Price weakness also affects the future supply picture through project execution. New refining plants, separations circuits, and chemical conversion lines are not switched on in response to short-term demand alone. They rely on financing confidence, permitting, engineering execution, reagent supply, power reliability, and qualification with downstream users. When prices soften, marginal projects often slow, even if long-run strategic demand remains intact. The visible market may look calm while the next layer of capacity quietly moves further out on the calendar.

That lag is particularly relevant in non-Chinese rare earth separation, graphite processing, and specialty by-product recovery. Pilot success does not always translate into commercial yield, impurity control, or steady throughput. In several markets, the discovery moment came after announcements: nameplate ambition was not the same as sustained, specification-compliant output. Supply risk interpretation so benefits from separating “announced,” “commissioned,” “qualified,” and “consistently delivered.” Only the last category resolves practical scarcity.

Observed response patterns and the trade-offs they reveal

Across industrial supply chains, several response patterns have appeared repeatedly. None removes risk entirely; each shifts it from one node to another. Diversification across jurisdictions reduces single-country exposure but can add qualification complexity. Holding more intermediate inventory can soften short-term disruption but does not solve structural refining dependence. Recycling and secondary feed can improve resilience in some products, yet quality consistency and traceability can become more important. Material substitution can help, but performance trade-offs are common, especially in magnets, high-spec chemicals, and impurity-sensitive applications.

- Geographic diversification: lower concentration risk, higher coordination and qualification burden.

- Multiple process routes: better flexibility, but more complex impurity and consistency management.

- Secondary and recycled feed: resilience benefits where recoverability and specification control are mature.

- Substitution or redesign: possible in selected applications, often constrained by performance and certification requirements.

- Structured monitoring: useful where trade policy, plant performance, and customs practice move faster than annual supply-demand studies.

Why critical mineral prices are so volatile

Critical mineral price volatility tends to be amplified by thin markets, uneven transparency, concentration of processing, policy intervention, and long project lead times. Many of these markets are small relative to bulk commodities, so inventory shifts or a single plant outage can move sentiment quickly. The chain is also chemically specific: small differences in purity, particle size, or precursor route can separate interchangeable material from non-interchangeable material. Volatility therefore reflects both commodity-market behavior and industrial qualification constraints. In rare earths and by-product metals, the signal is even noisier because supply can be dictated by another metal’s economics or by a state policy choice rather than by the standalone price series.

Procyon Metals maintains strategic metals monitoring across refining concentration, export-control exposure, project execution, and by-product dependency. Discussion requests regarding strategic metals monitoring, watchlists, and market-interpretation frameworks can be directed to Procyon Metals.