Across the US and Europe, rare earth project headlines now span mines, solvent-extraction plants, oxide capacity, metal conversion, alloy production, magnet manufacturing, recycling, and public-policy support. In operating reviews, the first discovery moment often appears early: a “rare earth supply” announcement describes only ore, concentrate, or mixed carbonate, while rare earth separation, metal-making, or magnet conversion remains external, conceptual, or dependent on another jurisdiction. That gap between headline scope and deliverable scope is the central issue in rare earth projects due diligence.

Key Takeaways

- Mine output and magnet supply are different industrial stages with different equipment, permits, qualification cycles, and failure modes.

- The strongest US rare earth supply chain and EU critical raw materials announcements usually specify product form, plant location, downstream dependencies, and documentary status rather than broad tonnage language alone.

- Rare earth separation is frequently the real bottleneck, especially where feed mineralogy, waste handling, radiological controls, and solvent-extraction know-how are unresolved.

- Metal-making, alloying, and magnet manufacturing introduce separate purity, ppm impurity control, and customer-qualification risks even after oxide production is established.

- Public support mechanisms, financing packages, and offtake announcements can improve visibility, but they do not erase permitting, commissioning, logistics, or technical scale-up risk.

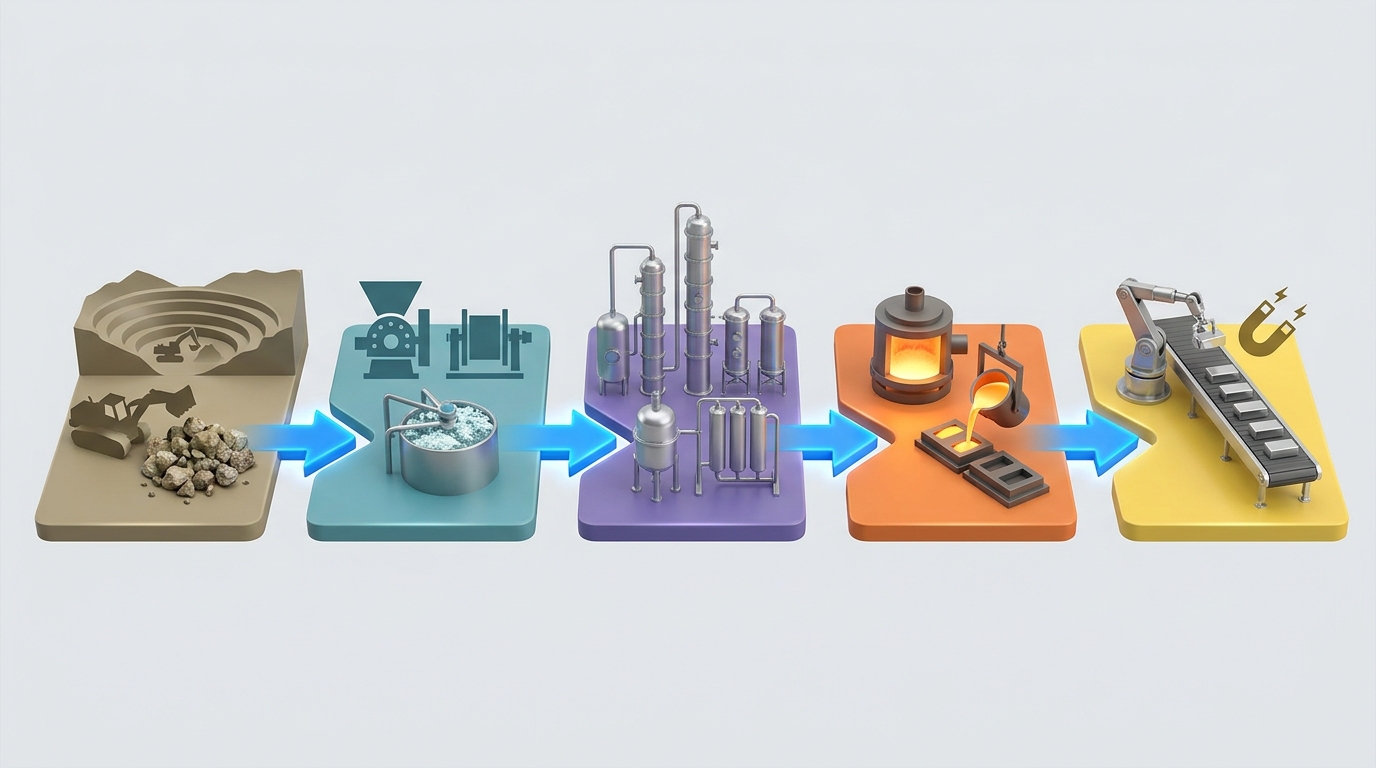

Why Mining Is Not the Same as Magnet Supply

Rare earth supply chains are sequential. Mining and beneficiation generate ore or concentrate, often described through TREO, or total rare earth oxide content. Separation then isolates individual oxides such as NdPr oxide, dysprosium oxide, or terbium oxide through complex chemical processing, typically using solvent extraction. Metal-making reduces those oxides into metal. Alloy production prepares feed for magnet manufacture. Magnet manufacturing itself adds powder handling, pressing, sintering, machining, coating, and end-customer qualification. A project can be successful at one stage and still leave the overall chain exposed.

This distinction matters because the strategic concern in Western announcements is rarely simple ore availability. The pressure point is much more often the ability to turn a mined material into specification-grade oxides, metals, alloys, and finished magnets inside reliable jurisdictions. In practice, a mine in the US with separation in a second country, alloy conversion in a third, and magnet manufacturing in a fourth still carries route risk, export-control risk, customs friction, traceability complexity, and schedule risk at every handoff.

A second discovery moment often emerges when “integrated” is used loosely. In some announcements, integration means a conceptual ambition across the value chain. In operational terms, integration means named plants, defined feedstock, tested flowsheets, qualified outputs, environmental permissions, and realistic handoff between stages. That distinction is easy to miss in headline reading and becomes obvious only when the value chain is mapped stage by stage.

A Practical Scope for Rare Earth Projects Due Diligence

A durable review framework usually begins with a narrow question: what exactly is being produced, where, and in what chemical or metallurgical form? Public announcements often compress several stages into one phrase such as “rare earth materials” or “magnet supply.” Analytical work becomes clearer when the output is identified precisely as concentrate, mixed rare earth carbonate, separated oxide, metal, alloy, magnet alloy feed, or finished magnet.

- Feedstock definition: deposit type, mineralogy, and whether the project is oriented toward light rare earths or includes meaningful heavy rare earth exposure.

- Process definition: beneficiation route, rare earth separation method, metal reduction route, alloy preparation, and whether magnet manufacturing is included or external.

- Product definition: which oxides or metals are planned, what purity is stated, and whether impurity control is discussed in ppm where relevant.

- Location map: mine, separation plant, metal plant, alloy site, magnet plant, recycling unit, storage, and shipping route by jurisdiction.

- Document set: pilot data, qualification data, environmental filings, water rights, waste permits, radiological handling plans, and customer testing evidence.

The documentary layer often reveals more than the headline. A resource statement without a flowsheet says little about recoverable, saleable product. A separation concept without pilot-scale evidence says little about solvent balance, waste chemistry, or actual oxide purity. A magnet manufacturing line without named alloy feed or customer qualification says little about commercial usability. In other words, the useful unit of analysis is not headline capacity but verified conversion from one stage to the next.

Where the US and EU Value Chain Commonly Tightens

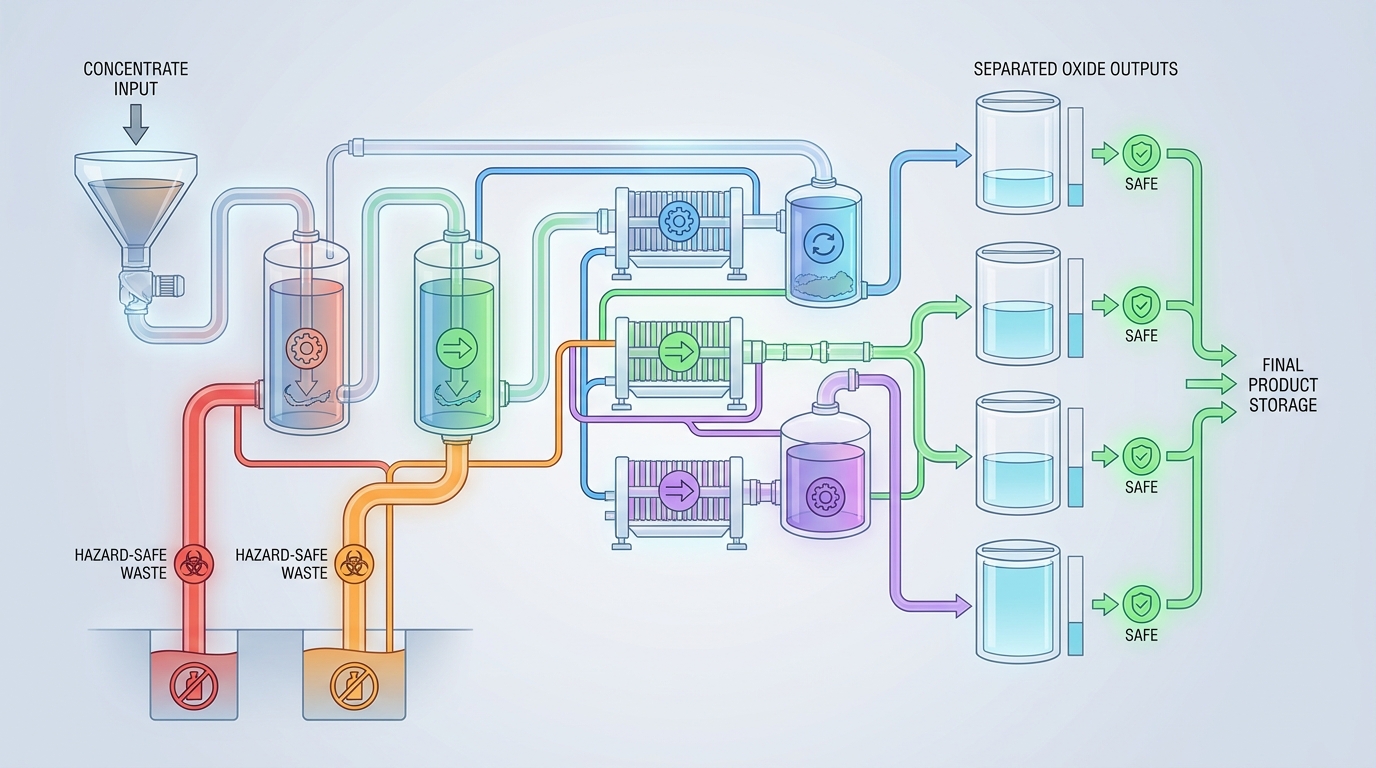

For the US rare earth supply chain and for EU critical raw materials planning, separation remains the most common pressure point. Rare earth separation is chemically demanding, environmentally sensitive, and operationally unforgiving. Feed variability can alter recoveries. Waste streams can change permit complexity. Thorium or uranium association in certain mineral systems can widen the compliance burden. An announcement that treats separation as a routine add-on to mining usually understates the real bottleneck.

Metal-making and alloying create a second, less visible bottleneck. Converting oxides to metal and then to magnet alloy is not a paperwork extension of separation. It is a distinct metallurgical capability with contamination control, oxygen management, process yield discipline, and customer qualification requirements. A plant may produce oxide successfully while still relying on imported metal or alloy feed. In practical terms, that means diversification remains partial rather than complete.

Magnet manufacturing adds another layer. Finished NdFeB magnets require not only metallurgical feed but process repeatability, machining quality, coating reliability, and performance validation for automotive, industrial, clean-energy, semiconductor, or defense applications. Public announcements sometimes present a magnet line as the endpoint of resilience, but magnet plants are only as secure as their alloy inputs, technical labor base, and qualified demand profile.

Permitting, Compliance, and Jurisdictional Friction

Permitting risk is rarely uniform across the chain. A mine, a separation plant, a metal facility, and a magnet plant each face different regulatory exposures. In the US, environmental review, state-level air and water permits, waste management, and site-specific litigation risk can move on different timelines. In Europe, environmental impact assessment, chemical handling, industrial emissions, water use, waste classification, and traceability obligations often shape the path from concept to commissioning. A single weak link in that stack can hold back the wider project narrative.

Observed in practice, one of the more important discovery moments appears when a project has advanced engineering at the mine or magnet stage but has only preliminary work at the chemical processing stage. The downstream plant frequently carries the more sensitive waste, water, or emissions profile. Another recurring issue is geographic fragmentation: ore in one jurisdiction, separation in another, and downstream magnet manufacturing elsewhere. Every crossing introduces documentation needs tied to export controls, sanctions screening, rules of origin, transport classification, and product traceability.

EU policy and US policy also frame risk differently. European critical raw materials policy places visible weight on strategic autonomy, sustainability, and resilience inside the bloc. US policy discussions more often emphasize security, industrial readiness, and domestic processing capacity. Both approaches matter in rare earth projects due diligence because a project may align politically with resilience goals while still carrying unresolved plant-level risk.

Offtake, Financing, and Market-Support Signals

Offtake and financing are often treated as proof of maturity, yet they function better as evidence categories than as conclusions. A long-term offtake announcement can indicate demand visibility, customer interest, or state-backed industrial alignment. It does not automatically prove that the product is qualified, that the volumes match realistic ramp-up, or that every intermediate stage exists. The same applies to financing language: committed funds, conditional support, public grants, export-credit backing, and strategic partnership memoranda carry very different implications for execution.

Recent policy debate in the US and Europe has also brought more attention to coordinated market-support mechanisms. Reference-price systems, border-adjusted price floors, price-gap subsidies, and long-term offtake arrangements are discussed as ways to keep non-Chinese projects from being undercut by lower-priced Chinese supply. These mechanisms matter because rare earth projects can be technically sound yet commercially fragile during adverse pricing periods. At the same time, policy support does not commission a plant, resolve a metallurgical problem, or compress a permit timeline.

Common Failure Modes Seen in Public Announcements

- The mine is real, but the project ends at concentrate or mixed carbonate rather than separated oxides.

- Separation is planned, but feed mineralogy, recoveries, or waste handling remain underdefined.

- Separated oxides are expected, but metal-making and alloy conversion remain dependent on imported intermediates.

- A magnet manufacturing line is announced, yet qualified alloy feed or customer acceptance is still absent.

- Permitting progress is concentrated at the least complex stage, while the chemically intensive stage remains early.

- Financing language is broad, but the funding stack is split across several facilities that need synchronized completion.

- Recycling is included rhetorically, although feed availability, contamination handling, and product specification are not yet visible.

What Tends to Matter More Than Headline Capacity

For family offices, strategic metals research teams, and private wealth advisors conducting commercial investigation, the clearest signal is specificity. A credible announcement usually defines the stage, identifies the plant, locates the jurisdiction, names the intermediate product, and shows how the next conversion step is handled. It also tends to acknowledge the non-mining bottlenecks: rare earth separation, metal conversion, alloying, magnet manufacturing, environmental compliance, and customer qualification. When those pieces are visible, the supply chain story becomes measurable. When they are absent, diversification is often more narrative than operating reality.

In that sense, the enduring question is not whether a rare earth project exists, but whether the chain from rock to magnet is actually continuous. Mining alone rarely answers that question. Separation, oxide purity, metal-making, alloy preparation, magnet manufacturing, permitting depth, logistics routes, and financing structure answer much more of it.

Organizations looking for a deeper internal review structure can request Procyon’s strategic metals project due diligence questions as a working framework for screening US and Europe rare earth announcements without headline distortion.