Securing Rare Earth Supply: Strategic Playbook for Business Leaders

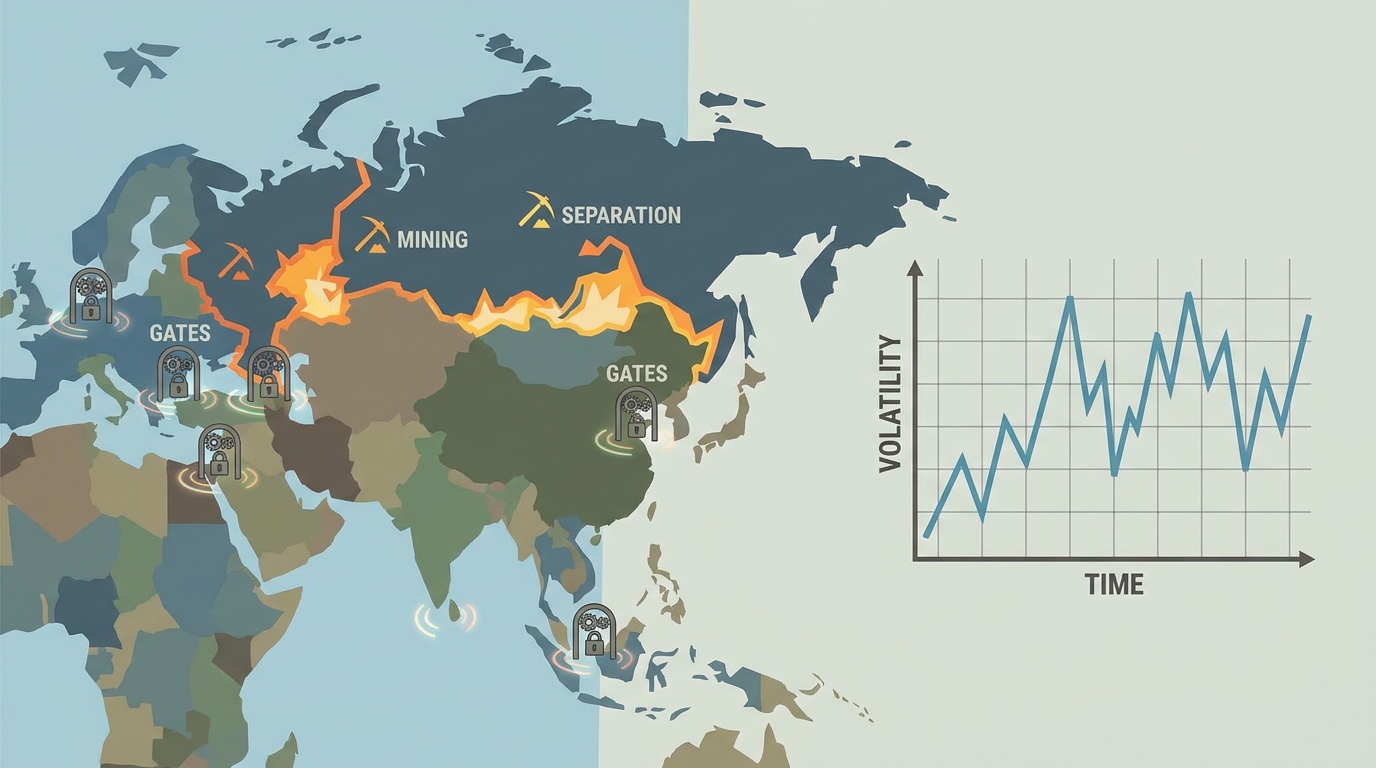

Why this matters: As electric vehicles, wind turbines, robotics, and defense systems proliferate, securing neodymium, praseodymium, dysprosium, and terbium becomes a board‐level mandate. Price spikes from $80 to $200/kg in under six months (Fastmarkets, 2026) and shifting export quotas (China Mof, 2025) show that supply shocks can erode margins, delay product launches, and trigger stakeholder backlash.

Executive Summary

Business leaders face two intertwined risks in rare earths: cost volatility and supply concentration. This guide translates technical points into tangible actions—mapping exposure, structuring contracts, diversifying sources, and building midstream partnerships—to protect EBITDA, preserve launch schedules, and maintain competitive advantage.

1. Business Objectives: Defining Success

Your north star is secure access at acceptable cost and acceptable risk. Success for industrial buyers and investors looks like:

- Production continuity: Zero unplanned shutdowns due to magnet shortages.

- Margin stability: Reducing input‐cost variance by 50% versus benchmark indices.

- Negotiation leverage: 10–15% better pricing through multi‐year indexed contracts.

Example: A European wind‐turbine OEM secured a five‐year NdPr contract with a floor/ceiling pricing formula, cutting cost spikes by 40% in 2026 (internal client data).

2. Investment Overview: Balancing Cost, Time & Resources

Building resilience is a multi‐year commitment. Allocate resources across three horizons:

- Short‐term (0–6 months): Supply‐chain mapping, benchmark subscriptions, and contract review. Estimated budget: $50K–$150K for market intelligence and legal fees.

- Medium‐term (6–18 months): Dual‐source qualification, test batches, ESG audits, and safety‐stock build‐up. Example investment: $1–2M yields 3–4 months of cover for key magnets.

- Long‐term (18–60 months): Equity stakes or offtake in separation, recycling, or magnet plants. A 5% stake in a midstream partner can unlock priority allocations and 0.5–1% EBIT uplift annually.

Industry outlooks project 15% annual growth in magnet demand through 2030 (BloombergNEF, 2024). Yet non‐China capacity remains under 20% of total (Lynas ~10%, MP Materials ramping; industry estimate, 2024).

3. Implementation Roadmap

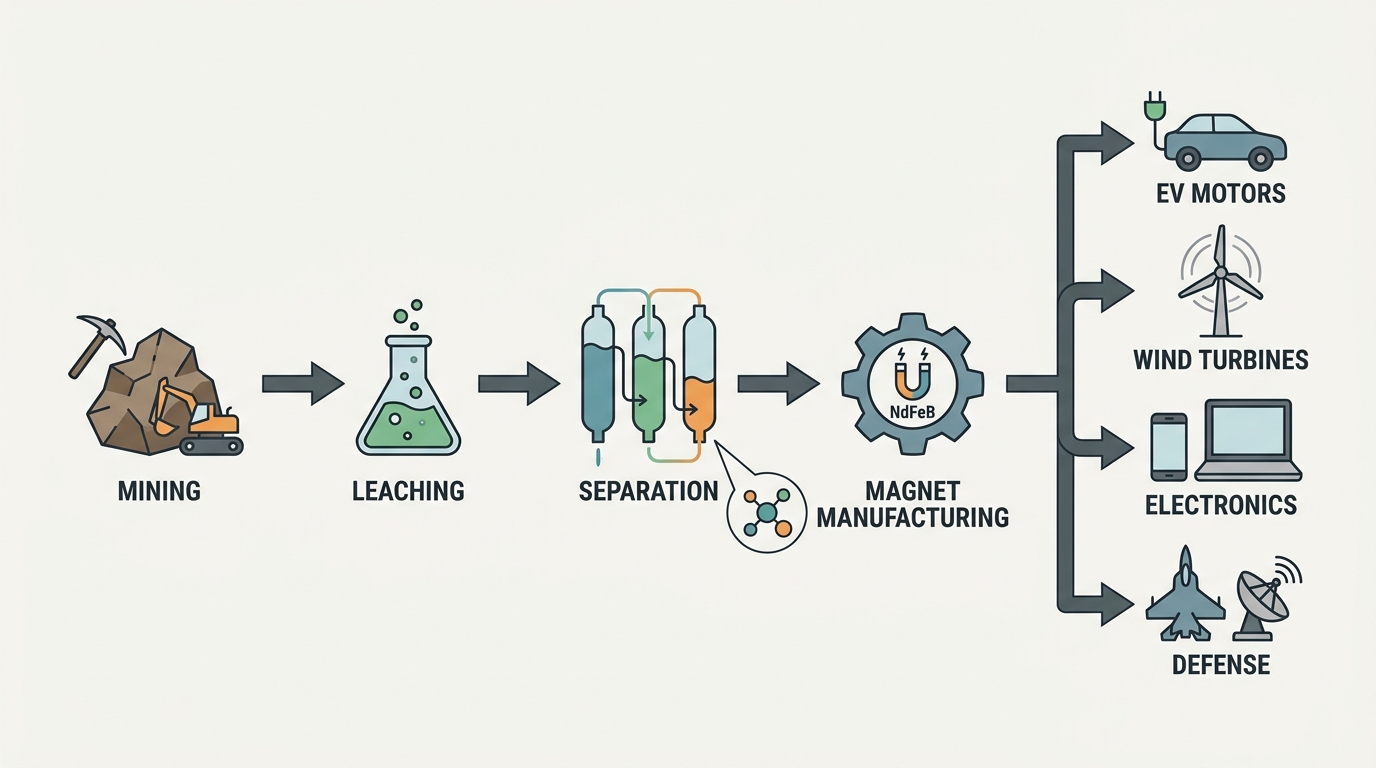

- Map Exposure: Identify every product and supplier that uses NdPr, Dy, Tb or their alloys. Build a tier‐three supplier register with geographies and lead times.

- Build Market Visibility: Track Shanghai Metals Market and Fastmarkets benchmarks, China quota announcements (20–30% swings), and U.S. Defense Logistics stockpile levels.

- Create Supply Optionality: Qualify at least two non‐China suppliers for each critical material. Negotiate indexed pricing clauses with caps/floors and allocation rights.

- Strengthen Midstream: Partner in separation, recycling, or magnet assembly. Establish memoranda of understanding (MOUs) with timelines and performance milestones.

Case in point: An automotive OEM reduced project delays by 20% after co‐investing in a U.S. recycling pilot, securing 10% of its 2028 NdPr needs at fixed fees.

4. Risk Mitigation: Common Pitfalls

- All rare earths are not the same: Report NdPr, dysprosium, and terbium separately—light vs. heavy elements carry different bottlenecks and price dynamics.

- Mine capacity ≠ usable supply: Verify separation, alloy, and magnet‐making capacity plus customer qualification status.

- Overreliance on China: Build regional alternatives in Australia, North America, or Southeast Asia and scenario‐test quota reductions.

- ESG oversights: Include environmental, social, and waste‐handling diligence—shutdowns often begin with regulatory or community pushback.

- Average pricing traps: Use trigger‐based governance: NdPr spikes above planning bands or quota cuts should auto‐escalate to finance and procurement heads.

5. Success Metrics & Dashboard

Measure leading indicators, not just spend:

- Supply visibility: % of rare earth exposure mapped through tier‐two and tier‐three suppliers.

- Diversification: % of NdPr, Dy, Tb from qualified non‐China sources.

- Inventory resilience: Months of cover for magnet‐critical materials.

- Contract quality: % of spend under multi‐year agreements with clear pricing formulas and force majeure terms.

- Lead‐time stability: Variance in magnet/component lead times versus plan.

- ESG traceability: Audit completion rate and remediation actions.

- Circularity: Recycled or recovered material share.

Example dashboard trigger: NdPr > $160/kg for 10 consecutive days → invokes emergency procurement review.

6. Partner Selection: Criteria for Success

- End-to-end expertise: From ore to magnet, with deep understanding of bottlenecks at each step.

- Market intelligence: Real-time tracking of pricing, quotas, ramp-ups, and demand proxies like EV production.

- Commercial structuring: Proven offtake agreements, indexed pricing, inventory strategies, and supplier‐qualification support.

- ESG & regulatory competence: Expertise in radioactive residue, permitting, and traceability requirements.

- Global reach: Regional insight across China, Australia, Southeast Asia, North America, and Europe.

- Board-level communication: Translating complexity into actionable capital allocation and risk‐management decisions.

Red flag: Advisors promising a “quick exit” from China or treating mine ownership as a complete strategy.

Conclusion & Next Steps

Rare earth materials are strategically valuable because separation, refining, and magnet production remain concentrated and complex. Business leaders win by treating rare earths as a continuity‐of‐supply ecosystem, not a simple commodity play. Prioritize visibility, diversify suppliers, structure robust contracts, invest in midstream optionality, and monitor triggers to act before shortages hit the P&L.

Schedule a Board-Level Briefing or Download Our Supply Chain Risk Checklist to kick-start your resilience program today.