Rare earth disruption rarely starts at the mine face. In operating reviews, the first fracture often appears further downstream: separated oxide allocation, metal-making, alloy conversion, sintered magnet production, or export paperwork tied to a jurisdiction that was not obvious in the original supplier map. That pattern matters for neodymium, praseodymium, dysprosium, and terbium because exposure is usually created by magnets and high-temperature performance requirements, not by the broad “rare earths” label alone. In practice, a mine outside China does not automatically remove China-linked risk if separation, metal conversion, or magnet finishing still runs through Chinese capacity or through trading routes with incomplete origin documentation.

Key takeaways

- Rare earth supply risk sits in the full chain: ore, separation, metal, alloy, magnet, component, and export documentation.

- NdPr exposure usually tracks electric motors and high-performance magnets, while dysprosium and terbium exposure is concentrated in heat-resistant magnet applications such as aerospace, defence-adjacent systems, and some industrial drive environments.

- A sourcing mix with more than 70% China-linked material is commonly treated as high concentration risk, especially when heavy rare earths depend on Chinese separation or licensing channels.

- Observed failure modes include purity drift, hidden midstream dependency, incomplete traceability, customs delays, and inventory signals that arrive too late to prevent line disruption.

- Common management structures include supplier diversification, indexed supply formulas, tolling or midstream partnerships, recycling flows, and documented origin controls; each reduces one part of the problem rather than the whole problem.

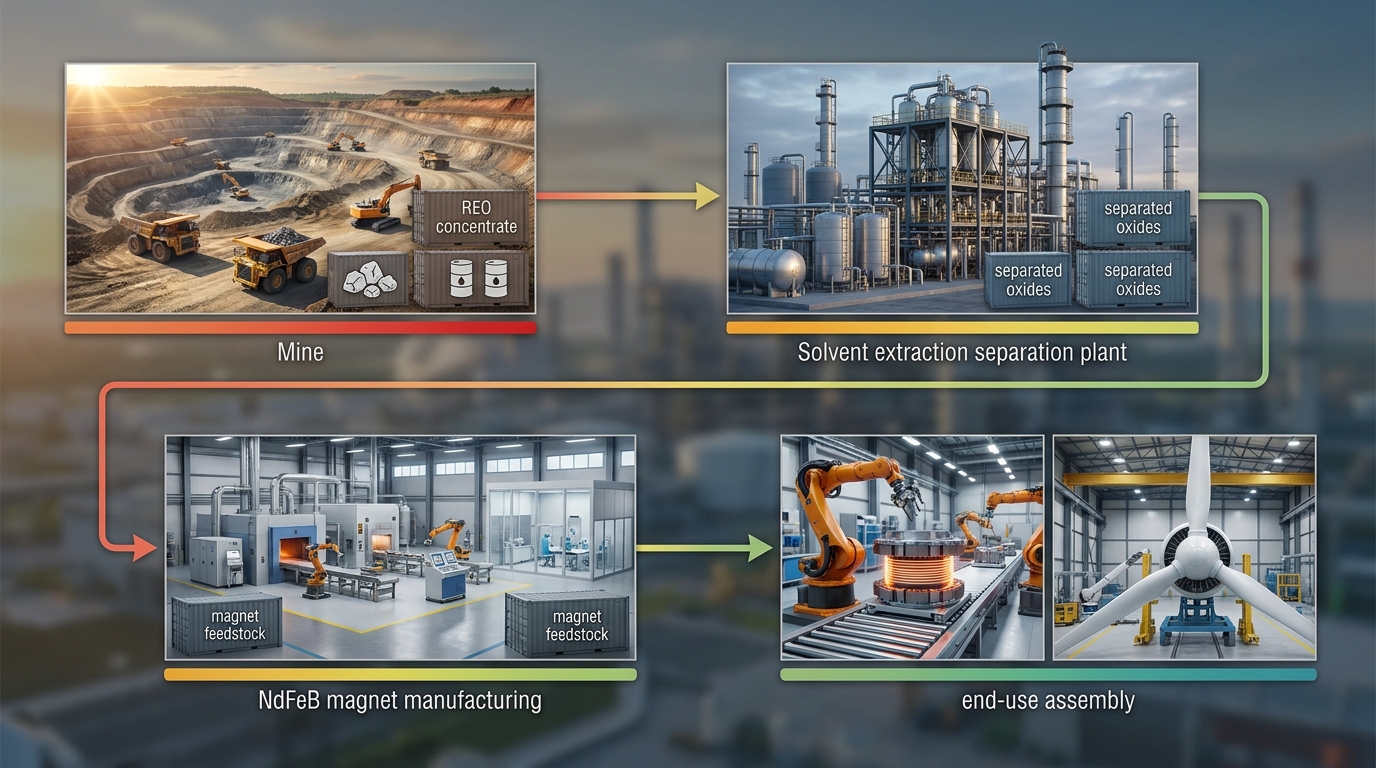

Rare earth elements explained through end uses and processing steps

The rare earth supply chain is often described as a mining story, but commercial exposure is usually a magnet story. Neodymium and praseodymium are commonly grouped as NdPr because they are central to NdFeB permanent magnets used in traction motors, wind turbine generators, robotics, and compact industrial drives. Research notes used in procurement screening often cite roughly 5-10 kg of NdPr per metric ton of EV motor-related output, although actual loading varies by motor design, power density, and the extent of ferrite or induction alternatives. Dysprosium and terbium matter for a narrower but more fragile slice of demand: magnets that need thermal stability and coercivity in higher-temperature operating environments.

That distinction changes the way risk is measured. A business may appear diversified on total rare earth inputs while remaining highly exposed on magnet metals. Another discovery from field reviews is that oxide availability and magnet availability are not interchangeable. A supplier may have concentrate or mixed carbonate, yet no assured separation slot, no metal conversion route, or no qualified alloy partner. In other words, “rare earth metals explained” in operating terms means tracking the conversion path from TREO in concentrate to separated oxide, then to metal, alloy, magnet, and finished component.

Where concentration risk actually sits

China-linked concentration remains the central structural feature of the global rare earth supply chain, especially in separation, metal-making, and magnet manufacturing. In internal risk dashboards, one frequently used marker is simple: more than 70% China-linked sourcing is flagged as high concentration risk. The reason is not only market share. It is the combination of processing dominance, licensing discretion, and the ability of administrative controls to create multi-month timing gaps even when physical material exists.

Heavy rare earths show this most clearly. Public reporting around 2025 highlighted tighter export licensing for dysprosium and terbium-related flows. Exact delays vary by shipment, counterparty, and end use, but the operating consequence is familiar: lead times stop behaving like logistics and start behaving like regulatory queues. A second recurring discovery is route concentration. Material mined in Australia, the United States, or Canada may still pass through Malaysia for processing, or through Chinese metal and magnet converters, before reaching an OEM or tier supplier. The map looks diversified until the midstream is drawn in full.

Risk criteria used in supplier qualification

Supplier qualification in this category is less about a single vendor questionnaire and more about evidence across five layers.

- Material quality: ore grade and TREO composition at the mine, then magnet-grade purity at oxide and metal stages. A recurring failure point is assuming that available oxide automatically meets metal or alloy purity needs. In magnet applications, purity above 99.5% is often referenced for critical conversion stages.

- Capacity realism: nameplate capacity, actual operating output, maintenance downtime, reagent dependency, and commissioning maturity. Development-stage assets and ramping separation plants sit in a different risk class from stable commercial operations.

- Traceability and origin: documented chain of custody, beneficial ownership, and processing location. UFLPA screening, sanctions exposure, REACH documentation, and defence-related controls such as ITAR can become decisive.

- Midstream dependency: separation partner, metal-making route, alloy producer, and magnet finisher. This is where many non-China narratives break down under scrutiny.

- Logistics and customs resilience: port dependence, transshipment nodes, residue handling constraints, customs classification, and completeness of export licensing files.

Publicly visible non-China nodes often examined in this framework include Lynas in Australia and Malaysia, MP Materials in the United States, and selected Canadian or Australian heavy rare earth projects such as Nechalacho and Browns Range. The important analytical point is not supplier branding; it is the exact stage reached commercially. Some assets provide concentrate. Others provide separated oxide. Fewer provide metal, alloy, or magnet output at scale.

Failure modes observed in practice

- Purity mismatch: the purchased form meets assay expectations at one stage but fails in alloying or magnet sintering. This is common where qualification focused on TREO rather than final-use chemistry.

- Hidden China exposure: the primary supplier sits in a non-Chinese jurisdiction, but solvent extraction, metal conversion, or magnet finishing remains China-linked.

- Documentation failure: origin records, environmental permits, or export classifications are incomplete, causing customs holds or compliance escalations.

- Single-route logistics: one port, one processor, or one transshipment hub carries the entire flow. Malaysia-related residue scrutiny and permitting debates have shown how non-mine issues can become supply issues.

- Inventory blind spots: supply-days-on-hand falls below 90 before management visibility catches up. By that stage, the problem is no longer procurement timing alone; it becomes production scheduling.

A notable discovery from disruption reviews is that heavy rare earth shortages often surface first as allocation behaviour rather than outright force majeure. Suppliers preserve strategic accounts, product grades narrow, and informal lead-time guidance stops matching actual shipment release. That pattern is easy to miss when dashboards track only price or only warehouse stock.

Observed management structures across procurement and midstream

Market practice shows several recurring approaches, each attached to different failure modes. Supplier diversification is the most visible, but it is only meaningful when diversification exists at the same processing stage as the exposure. For NdPr, that may mean one source of separated oxide in Australia-linked flows, another in the United States, and a separate metal or alloy path if magnet conversion remains concentrated. For dysprosium and terbium, the analysis is stricter because heavy rare earth alternatives are fewer and project maturity outside China is more limited.

Contract structures also vary by stage. Observed forms include index-linked oxide or metal formulas, floor-and-collar arrangements, force majeure language tied specifically to export licensing, and take-or-pay structures where a processor needs volume certainty to reserve separation capacity. These structures can smooth volatility or improve allocation visibility, but they do not eliminate physical concentration. A contract tied to a supplier without secured midstream capacity simply converts market risk into performance risk.

Midstream partnerships are so a separate analytical category. Tolling arrangements, dedicated separation campaigns, alloy conversion partnerships, and magnet recycling loops all appear in current rare earth resilience planning. Public examples include Lynas-linked separation development in Texas and MP Materials’ effort to extend beyond concentrate into separated NdPr and downstream magnet material. The broader point is operational: midstream control changes the risk profile more than mine ownership alone. Recycling and scrap recovery add another layer, particularly for NdPr from end-of-life magnets, although scrap chemistry, contamination, and qualification cycles often limit immediate substitution.

Risk metrics and signals worth tracking

- China-linked share of total sourcing: above 70% is widely treated as a high-risk concentration marker.

- Quarterly volatility: coefficient of variation above 30% indicates unstable pricing conditions even before physical shortages become visible.

- Supply-days-on-hand: below 90 days is a common alert threshold in magnet-metal planning.

- Separated-outside-China share: a more revealing metric than mine-origin share alone.

- Compliance completeness: percentage of volume with auditable origin, sanctions screening, UFLPA review, and end-use documentation.

- Lead-time drift: rising variance matters as much as rising average lead time when export licensing is the bottleneck.

External benchmarks such as USGS criticality discussion, public company operating reports, customs notices, and specialist market services help frame the market, but internal BOM data often provides the decisive signal. A small share of total spend can still represent a single point of failure if that share carries all magnet performance or temperature resilience.

How resilience appears in real rare earth operations

Operationally resilient rare earth programs tend to show a few common characteristics: exposure mapped by metal rather than by broad commodity family; at least one verified non-China route at the same processing stage as the risk; quality evidence that reaches final-use requirements rather than mine assay only; and documented awareness of where dysprosium and terbium enter the design. Some sectors also explore engineering pathways that reduce heavy rare earth intensity, but those pathways are often constrained by qualification cycles, thermal performance needs, and customer approvals.

For business leaders reviewing rare earth supply security, the core analytical shift is straightforward. The relevant question is rarely “Is there a supplier?” The more accurate sequence is “At which stage is concentration highest, which documents unlock movement, where does purity actually matter, and which disruption arrives first in practice?” In rare earths, resilience is usually built or lost in those details.