Operationally, rare earth disruptions rarely begin with the headline narrative around electrification, defense demand, or strategic materials. They usually begin much earlier: a concentrate that behaves differently in pilot work than in the flowsheet, an impurity profile that complicates solvent extraction, an oxide that misses customer purity expectations, or a magnet qualification program that runs longer than the upstream project assumed. In practice, the central distinction is not “rare earth demand is strong” versus “rare earth demand is weak.” The meaningful distinction is whether a supply chain node has moved from geological promise into repeatable industrial performance.

Key takeaways

- Rare earth resilience is usually determined less by resource size than by recoverable NdPr content, impurity handling, separation capability, and qualification with downstream users.

- Mine-to-magnet integration can reduce dependency on external processors, but each additional step introduces new commissioning, compliance, and quality-control risk.

- Many juniors stall between pilot data and commercial supply because metallurgy, permitting, radionuclide management, or financing assumptions fail to scale together.

- Offtake agreements and government backing are informative only when linked to product specification, qualification status, documentary obligations, and a credible project sequence.

Analytical scope: what is actually being evaluated

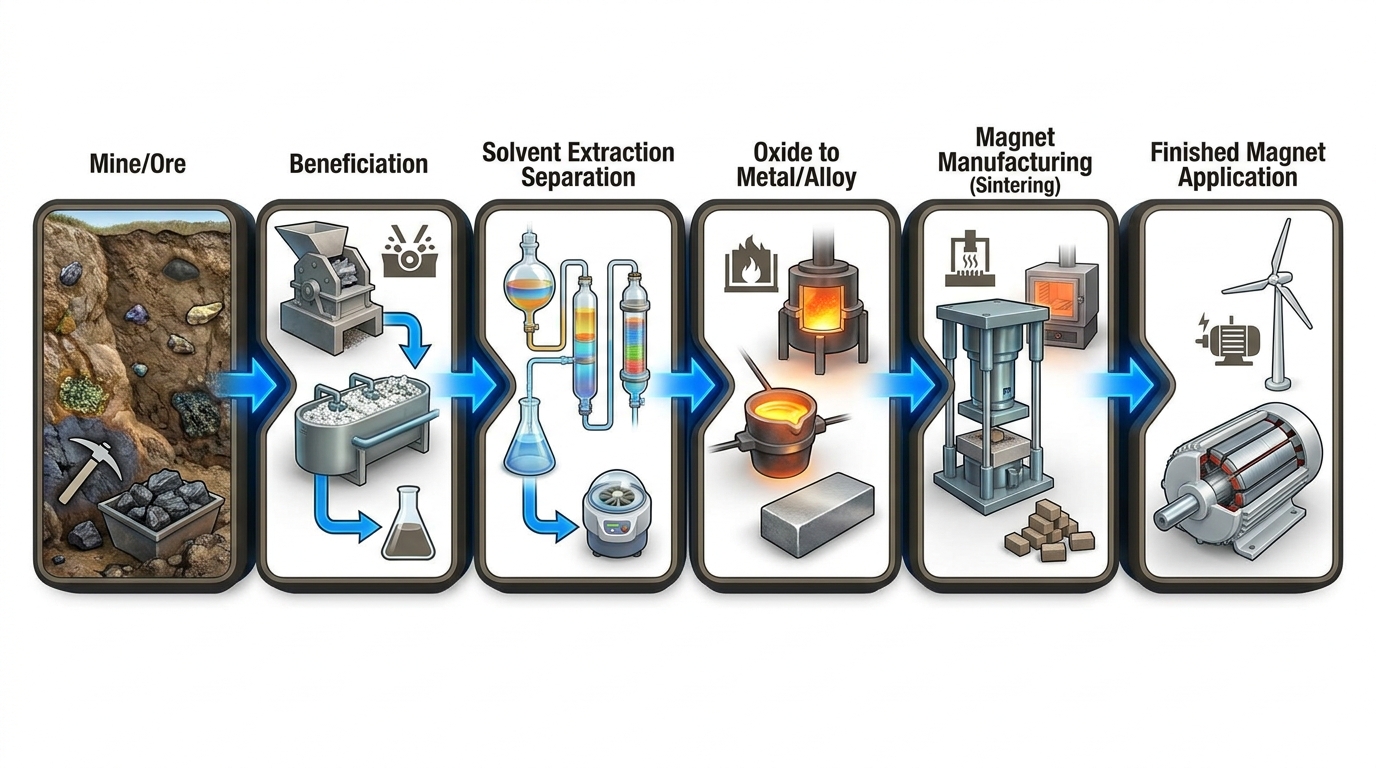

A useful analytical frame treats a rare earth company or project as a chain of dependent industrial steps rather than as a single mining asset. The relevant unit of analysis is often the full path from ore to separated oxides, then to metals, alloys, and in some cases magnets. That path matters because total rare earth oxides, or TREO, can overstate commercial relevance when the recoverable magnet basket is narrow or when heavy processing is needed before saleable material exists. In most industrial applications, the focus remains on NdPr for permanent magnets, with dysprosium and terbium adding value where heat resistance matters.

In observed supply chains, the main jurisdictions often play different roles. China remains central in separation and magnet manufacturing. Australia has hosted important mine development and concentrate supply. Malaysia has appeared in intermediate processing routes. The United States, Japan, and the European Union have increasingly emphasized downstream qualification, public support, and alternative processing capacity. That geographic split means the same project can appear robust at mine level yet remain exposed at the separation or magnet stage.

The most informative review generally breaks the system into five criteria: ore quality and mineralogy, processing proof, compliance and documentation, downstream qualification, and geopolitical exposure. A recurring discovery moment in practice comes when an attractive TREO figure is revisited after recoveries, gangue behavior, radionuclide handling, and customer purity requirements are layered onto the original story. The commercially relevant stream often becomes much narrower than the early resource narrative suggested.

Criteria that separate a supply-ready asset from a promotional one

The first criterion is mineralogical tractability. Rare earth chemistry is rarely forgiving. Monazite, bastnäsite, ionic clay feed, and other host types do not scale in the same way, and the presence of thorium, uranium, phosphate, or iron can reshape the whole processing route. Laboratory recoveries are informative, but pilot-scale continuity often reveals the real difficulty: reagent intensity, phase instability, residue management, and oxide purity drift. Where only bench data exists, operational uncertainty usually remains high.

The second criterion is separation evidence. Mining and concentration are only the beginning. Commercial readiness depends on whether mixed rare earth streams can be separated into saleable oxides at consistent purity. This is where many projects encounter the hidden bottleneck. Solvent extraction circuits are complex, contamination can migrate across stages, and small deviations in feed chemistry can alter product quality. In practice, a project with modest mining simplicity but strong separation proof can be more resilient than a larger deposit that still relies on third-party processing assumptions.

The third criterion is documentary and compliance readiness. Observed burdens often include certificates of analysis, chain-of-custody records, origin documentation, radionuclide handling plans, transport classification, chemical registrations such as REACH in Europe where relevant, and customer-specific traceability packages. For defense-linked or strategic applications, end-use scrutiny may also expand. Rare earth projects sometimes appear technically ready but remain commercially constrained because product traceability and compliance records lag behind physical production.

The fourth criterion is downstream qualification. Magnet supply chains are specification-driven. An oxide can meet an internal assay target and still fall short in a metal, alloy, or magnet plant because impurity tolerances are tight and process stability matters as much as headline purity. One of the clearest practical dividing lines is whether material has moved beyond engineering samples into sustained qualification with named downstream counterparties. That evidence usually carries more weight than broad statements about future demand.

The fifth criterion is structural exposure across jurisdictions. A mine in a stable jurisdiction may still depend on separation capacity in another region, shipping routes with export-control sensitivity, or a magnet customer base concentrated in one country. The supply chain so needs to be mapped by node, not by mine location alone. Concentrate routes, toll processing arrangements, and final magnet conversion can each reintroduce geopolitical risk even after upstream diversification appears complete.

Failure modes repeatedly observed in rare earth development

Several failure modes recur with unusual consistency. The first is the metallurgy gap: a project moves from attractive geology into pilot work and discovers lower recoveries, more difficult impurity rejection, or a less favorable NdPr yield than the original narrative implied. The second is the scaling gap: unit operations function individually but fail to integrate into a stable commercial sequence. Rare earth projects often look coherent on a flowsheet long before they look coherent in a continuous plant.

A third failure mode is radionuclide and residue management. Monazite-linked projects in particular can carry thorium or uranium handling burdens that reshape permitting and waste strategy. This is not a side issue. It can influence site design, transport approvals, community acceptance, and the choice between domestic processing and export to an established processor.

A fourth failure mode is the qualification lag. In many industrial materials chains, commercial announcements arrive before the product is truly interchangeable with incumbent supply. Rare earths are a clear example. Oxides, metals, and magnets may each require distinct qualification. Where the public narrative focuses on “production” but downstream acceptance still sits in testing, the supply chain remains exposed to delay. This is one reason many juniors never reach meaningful production despite years of apparent progress: the process plant, the documents, and the customer qualification path do not mature at the same pace.

A fifth failure mode is capex timeline reality. Rare earth projects frequently expand in scope as they move from mine-only plans to separation, metal making, or full mine-to-magnet integration. Each expansion can be strategically understandable, yet it also changes plant complexity, construction sequencing, and commissioning burden. In operational terms, the difficulty is not merely the size of capex; it is the widening gap between an early development timetable and the later reality of engineering, permitting, commissioning, and product qualification.

Offtake agreements, government backing, and the meaning of “strategic”

Offtake agreements are often treated as shorthand for validation, but their analytical value varies widely. In practice, the main distinctions are whether the arrangement is binding or non-binding, whether product specifications are defined, whether qualification remains a condition precedent, and whether the counterparty is a true end user, a trader, or a strategic intermediary. A recurring discovery moment appears when an announced offtake is reviewed closely and turns out to be contingent on future permits, future plant completion, or future product testing. The label alone rarely resolves commercial risk.

Government backing also requires nuance. Public support in the United States, Japan, Australia, and the European Union has increasingly appeared in critical minerals and strategic processing initiatives. The resilience impact is strongest when backing is specific: project financing support, grants for downstream buildout, strategic procurement, export-credit participation, or public facilitation of permitting and infrastructure. The resilience impact is much weaker when the support is rhetorical or politically visible but operationally undefined.

The term “strategic” is therefore best interpreted carefully. Strategic relevance can improve access to institutions and counterparties, but it does not erase technical risk. A project may be highly relevant to non-China supply diversification and still remain fragile if separation evidence is limited, if qualification is incomplete, or if documentary compliance is underdeveloped.

Observed risk-management configurations in the sector

Several operating patterns appear repeatedly where resilience has improved. One is staged integration: concentrate first, then separation, then metals or magnets after customer qualification strengthens. Another is toll processing or partner processing during early years, which can reduce exposure to building every downstream step at once, although dependency on third-party capacity remains. A third pattern is jurisdictional diversification, where mining, separation, and magnet conversion are distributed across allied or lower-risk regions rather than concentrated in one country.

Additional configurations include mixed customer portfolios across industrial and strategic users, downstream joint ventures for metal or magnet conversion, and public-private structures where government backing supports a difficult early phase that private capital alone often avoids. Inventory buffering and dual-route qualification also appear in some supply chains, especially where one route relies on China-linked processing and another route is being developed in the United States, Japan, Europe, or Australia. None of these configurations removes technical risk; they mainly redistribute it across time, counterparties, and jurisdictions.

Mine-to-magnet integration deserves separate treatment because it is frequently presented as the end-state for resilience. Operationally, it can indeed improve traceability, reduce third-party dependence, and make a supplier more relevant to industrial policy. Yet each added step creates a new failure surface: oxide purity, metal losses, alloy consistency, sintering behavior, coating performance, and end-product qualification. The integrated story is strongest when each stage is evidenced independently rather than assumed to follow automatically from an upstream resource.

Closing frame

The rare earth sector tends to reward analytical discipline more than thematic enthusiasm. The practical question is rarely whether rare earths matter. Their role in magnets, defense systems, robotics, and electrification is already well established. The practical question is whether a given project or supplier has crossed the industrial thresholds that convert TREO in the ground into qualified material in a customer process. Once the analysis is framed that way, the decisive signals usually become clear: recoverable magnet content, separation proof, documentary readiness, real qualification, credible offtake structure, specific government backing, and a project sequence that respects capex timeline reality.