Publication setting: lang-en. This guide is written for family offices, strategic metals investors, and private wealth advisors reviewing heavy rare earth exposure through a supply-chain and resilience lens rather than a promotional one. The operational context is straightforward: many magnet supply chains appear diversified at the mine level, yet become highly concentrated once dysprosium and terbium are isolated, refined, and qualified for high-temperature use.

- Heavy rare earths matter less for bulk tonnage than for performance at heat, speed, vibration, and long duty cycles.

- Dysprosium and terbium are not interchangeable with neodymium and praseodymium in high-temperature magnet applications; they solve a different physics problem.

- The strategic bottleneck usually sits in ionic clay feedstock, separation capability, and qualification data, not in headline rare earth resource size alone.

- Recent disruption signals have centered on Myanmar feedstock routes into China, Chinese export control tightening, and slow non-China separation buildout.

- Observed resilience configurations include recycling, alternative refining geographies, stockpiles, and engineering approaches that reduce HREE intensity where thermal limits allow.

Why dysprosium and terbium matter more than their volume suggests

In permanent magnets, the central concept is coercivity. In plain English, coercivity describes how well a magnet resists losing its magnetic strength when exposed to heat or opposing magnetic forces. A standard NdFeB magnet can be very strong at room temperature, yet far less stable once temperature rises and mechanical stress becomes continuous. Dysprosium and terbium are used in small amounts to improve that stability. Their role is disproportionate because the application often fails on thermal stability before it fails on basic magnet strength.

This is why heavy rare earths appear repeatedly in high-temperature systems. Sector research cited in the brief points to EV traction motors from Tesla and BYD as examples of compact, high-rpm designs where heat generation makes Dy/Tb-doped magnets important. The same pattern appears in offshore wind generators exposed to sustained operating temperatures and corrosive conditions, and in defense systems where demagnetization is not a tolerable failure mode. Reporting referenced French groups such as Safran, Thales, and MBDA in that context. A recurring discovery in supplier review is that a product may be described as “rare earth magnet material,” while the decisive question is actually whether the heavy rare earth content has been engineered and validated for the real thermal envelope.

Light versus heavy rare earths: the non-interchangeable point

Light rare earths and heavy rare earths are often grouped together in public discussion, but they sit differently in supply-risk analysis. Neodymium and praseodymium drive the core magnetic field in many NdFeB magnets. Dysprosium and terbium are then added when the magnet must continue to perform under higher temperatures or stronger opposing fields. In practice, that means the lighter rare earths support volume production, while the heavy rare earths often determine whether the component remains usable in demanding duty cycles.

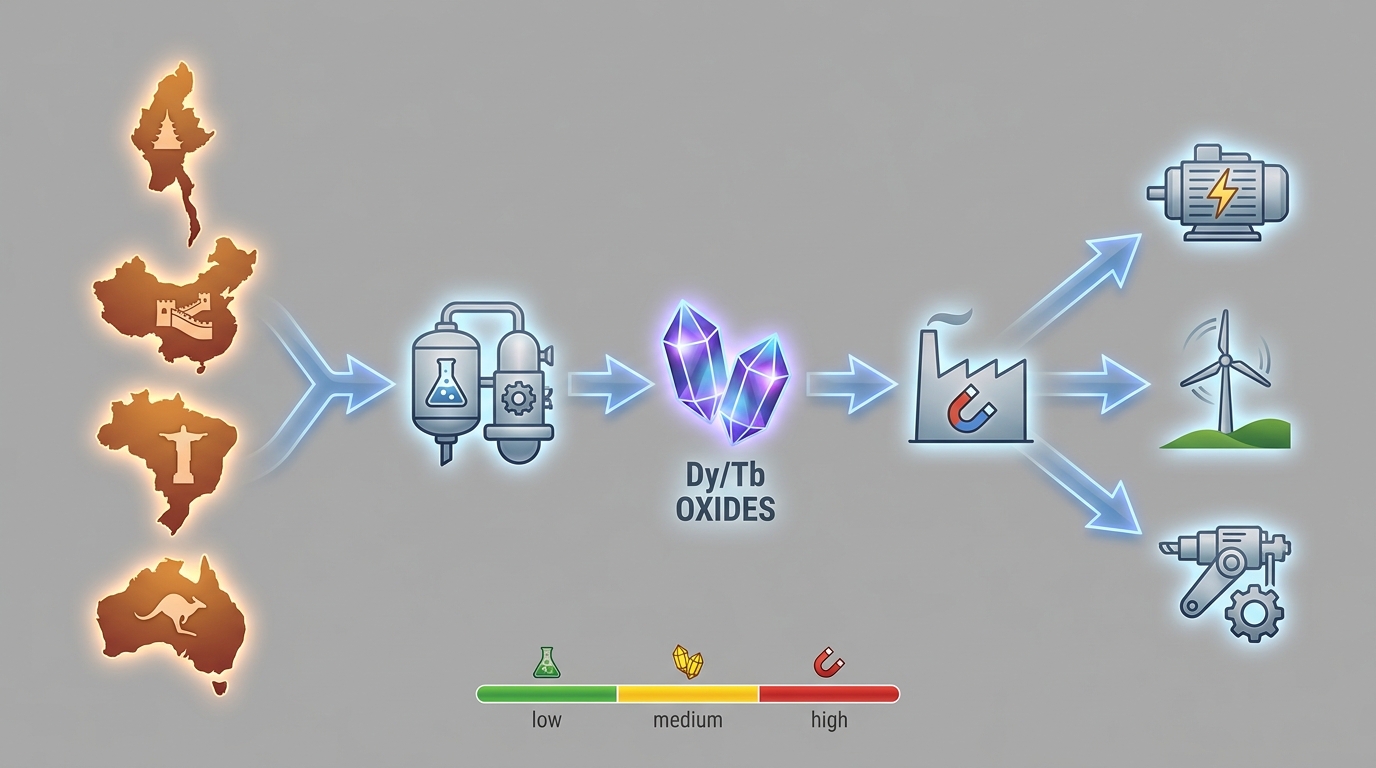

Geology reinforces that distinction. Light rare earths are more commonly associated with hard-rock deposits such as bastnäsite and monazite. Heavy rare earths are more strongly associated with ionic adsorption clays, especially in southern China and in Myanmar feedstock routes linked to Chinese processing. That difference matters because it changes everything downstream: mining methods, environmental controls, impurity profiles, traceability quality, and the availability of commercial separation capacity.

Where the bottleneck actually sits in the heavy rare earth supply chain

In operational terms, the heavy rare earth bottleneck is not a single choke point but a stack of dependencies. The first layer is feedstock origin: ionic clay material from Kachin State in Myanmar and from southern Chinese provinces such as Jiangxi and Guangdong remains central to global Dy/Tb availability. The second layer is chemical separation. Many projects can produce mixed rare earth material; far fewer can separate dysprosium and terbium to the purity required for magnet applications. The third layer is metallization, alloying, and magnet manufacturing, where small chemistry changes can alter high-temperature performance. The fourth layer is end-use qualification, where automotive, wind, and defense programs may reject material that is technically available but not yet validated.

An important discovery point in due diligence is the gap between “rare earth exposure” and “heavy rare earth capability.” A project can have a credible total rare earth resource and still offer limited near-term relevance to Dy/Tb-constrained magnets if the heavy fraction is small, difficult to separate, or routed to third-party processors. Another common discovery point is document asymmetry: mine presentations are often detailed, while separation flow sheets, impurity data, and magnet qualification records are much harder to obtain.

Evaluation criteria that clarify real supply risk

Four criteria tend to separate robust analysis from headline reading.

- Feedstock quality and mineralogy: The review focus is not only total rare earth oxide content, but the distribution of dysprosium, terbium, and related heavies within the ore or clay. Ionic clays and hard-rock deposits behave differently in processing and waste management.

- Separation capability: Mixed rare earth output is not equivalent to separated Dy and Tb oxides. The practical questions concern solvent extraction capability, impurity control, and whether the separation route is already operating at commercial scale or still sitting in pilot status.

- Thermal performance evidence: Magnet buyers in EV, wind, and defense systems care about coercivity retention under heat. Material qualification data matters more than generic claims of “high performance.”

- Traceability and compliance: Chain-of-custody records, assay certificates, environmental disclosures, and export-control exposure all influence whether the material is actually usable in regulated end markets.

Jurisdiction sits across all four. China remains dominant in heavy rare earth refining, and the brief highlighted that more than 70% of global dysprosium and terbium feedstock can trace back to routes that ultimately serve Chinese separation. Myanmar therefore matters beyond its own production footprint. Disruption in Kachin State is not a local mining issue alone; it can affect the availability of high-temperature magnet inputs globally. Non-China projects in the United States, Australia, Brazil, and Chile are strategically relevant because they change route optionality, even when they remain at pilot, ramp-up, or partial-processing stages.

Observed failure modes in heavy rare earth procurement and qualification

The first failure mode is thermal underperformance. A magnet can meet room-temperature specifications and still fail once the operating environment moves into the upper thermal band seen in traction motors, offshore wind equipment, or aerospace systems. The second failure mode is concentration risk disguised as diversification. Separate mines may still converge into the same refining geography, leaving the downstream chain exposed to one policy regime. The third failure mode is documentation weakness: incomplete assay records, unclear origin statements, or limited auditability around artisanal or informal clay extraction.

The latest developments reinforce those vulnerabilities. The brief referenced tighter Chinese controls on certain heavy rare earth and magnet exports in 2025, alongside rising trade friction with the United States. It also highlighted disruption in Myanmar, where conflict and border instability have affected feedstock flow. In practice, these developments tend to surface first as delays, qualification uncertainty, or changing allocation behavior rather than as a simple “no supply” event. Another observed failure mode appears in emerging non-China supply: mining progress can arrive earlier than separation readiness, producing a timeline mismatch between raw material availability and magnet-grade output.

Observed risk-management configurations across the market

Several patterns appear repeatedly in response to heavy rare earth concentration. One is geographic diversification of refining and magnet manufacturing, especially in the United States and Australia, even when feedstock remains globally mixed. Another is recycling: scrap magnets and end-of-life components are increasingly treated as secondary sources of dysprosium and terbium, although impurity management and collection quality remain important limits. A third pattern is engineering effort to reduce HREE intensity per unit of magnet performance, including more efficient use of Dy/Tb in magnet design where thermal margins permit.

A fourth pattern is strategic stockpiling in defense-adjacent systems, where continuity and qualification history often matter more than simple material availability. None of these configurations eliminates the bottleneck. What they do change is the location of the constraint: from raw material access, to separation capability, to qualification timing, to compliance management. That shift is often the practical difference between apparent supply and usable supply.

Two recurring questions in heavy rare earth analysis

Why are dysprosium and terbium important? Because they allow permanent magnets to retain performance under higher heat and stress. In EV motors, wind generators, and some defense systems, that thermal resilience can be more decisive than baseline magnetic strength.

What is the difference between light and heavy rare earths? Light rare earths such as neodymium and praseodymium are central to the main magnetic field and often dominate volume. Heavy rare earths such as dysprosium and terbium are scarcer and are used to preserve magnet performance when the operating environment becomes harsh. That is why heavy rare earths often form the strategic bottleneck despite far smaller tonnage.

In heavy rare earth due diligence, the most revealing evidence usually appears in feedstock origin, separation flow sheets, coercivity data, and qualification history rather than in total rare earth headlines. Procyon’s rare earth due diligence question set for heavy rare earth review is available on request.